The Week in 30 Seconds

- [MACRO] Fed flips hawkish. 9 of 18 FOMC members project a 2026 rate hike. Dot plot median up to 3.8%. Markets down 1.2%. 77% hike probability by December.

- [OIL] Oil crashes below $80. Brent hit $78.96 — first below $80 since March — on US-Iran deal. Geneva talks postponed Friday; oil bounced to $80.57. Weekly drop: 8.5%.

- [TECH] Intel-Apple US chip deal. Trump announced Apple will design and build chips with Intel in the US. Intel surged +10.5% to $133.82. No official confirmation yet.

- [SG] STI new all-time high. Singapore’s STI hit 5,226 on June 19 despite the hawkish Fed — Asia’s best-performing major index, +13.93% year-on-year.

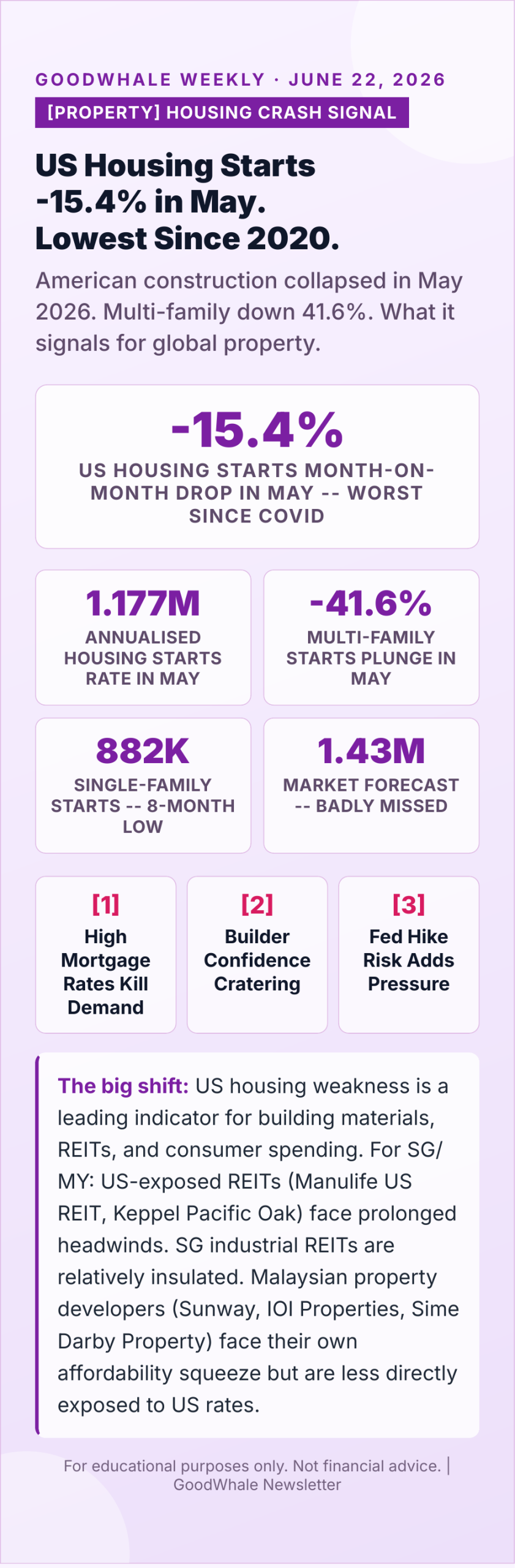

- [PROPERTY] US housing starts crash. Down 15.4% in May to 1.177M — lowest since May 2020. Multi-family down 41.6%. Signals sustained property weakness.

1. Fed rate hike 2026: Fed Rate Hike 2026: Warsh First FOMC Flips the Dot Plot Hawkish — The SG/MY Impact

Meanwhile, the Federal Reserve held its target rate at 3.50%–3.75% on June 17, 2026 in a unanimous 12-0 vote — but the market ignored the hold and focused entirely on the dot plot. In a major shift, 9 of 18 FOMC officials now project at least one rate hike before the end of 2026, with six of those pencilling in two 25-basis-point increases. The median year-end rate forecast jumped to 3.8%, up from 3.4% in March projections. The Fed also raised its year-end PCE inflation forecast to 3.6%, nearly double its 2% target. This is Fed rate hike 2026 territory — not a cut narrative anymore.

Markets moved fast. The S&P 500 dropped 1.21%, the Nasdaq fell 1.34%, and Treasury yields surged. Fed-funds futures moved to imply a 77% probability of a rate hike by December 2026, up sharply from just 24% a month ago. New Fed Chair Kevin Warsh kept his first press conference tight — the post-meeting statement was just 130 words, compared to 341 in April. The message was deliberate: data-dependent, no pre-commitment to direction. For SG/MY retail investors, the practical read is clear. SGD and MYR remain under steady USD pressure in a higher-for-longer, possibly higher-still world. SG REITs face prolonged borrowing cost headwinds — DPU compression and NAV pressure continue. USD T-bills at 4%+ remain the sensible parking spot. The earliest plausible easing is now 2027. If Warsh signals any dovish pivot — watch his July speeches carefully — that would be the moment to rotate dry powder back into SG REIT names like CICT and Mapletree Pan Asia Commercial Trust.

| FOMC Meeting | Rate Decision | Median 2026 YE Forecast | Hike Implied? |

|---|---|---|---|

| Jun 17, 2026 (Warsh #1) | Hold 3.5-3.75% | 3.8% | YES — 9/18 |

| Apr 29, 2026 | Hold 3.5-3.75% | 3.4% | No (cut implied) |

| Mar 18-19, 2026 | Hold 3.5-3.75% | 3.4% | No (cut implied) |

| Jan 28-29, 2026 | Hold 4.25-4.5% | 3.9% | Cuts implied |

2. Iran Deal Sends Oil Below $80 — The SG/MY Rotation Trade Every Investor Should Know

Notably, brent crude fell below $80 per barrel for the first time since March 2026 this week — closing at $78.96 on Monday as President Trump confirmed that a US-Iran peace framework had been signed, with oil sanctions relief taking effect immediately upon formal ratification. The deal would reopen the Strait of Hormuz, dismantle Iran’s nuclear programme, and lift the US naval blockade. That is the direct unwinding of a $30+ per barrel geopolitical premium that had been baked into crude since the conflict escalation in early 2026. The weekly decline of 8.5% erased most of the year’s conflict-driven gains in a single week.

There is a catch. On Friday June 19, US-Iran talks in Geneva were abruptly postponed, and Brent bounced back to $80.57. The deal is not yet final. But the direction of travel is clear, and the rotation trade is forming. If confirmation comes: reduce or hold Malaysian energy names — Hibiscus Petroleum, Bumi Armada, Petronas Chemicals — which have been direct beneficiaries of elevated oil. Add airlines, particularly Singapore Airlines (SIA) and Capital A / AirAsia, which have been squeezed by jet-fuel costs all year. Lower Brent also reduces MY’s fuel-import bill, which strengthens the ringgit. And lower energy is one of the most direct disinflationary forces in the global economy — if it holds, it actually gives the Fed reason to not hike in December. The oil-Fed feedback loop is the macro trade of the second half of 2026.

3. Intel-Apple US Chip Deal: Trump Announcement, INTC +10.5% — What SG/MY Investors Should Do

However, on Thursday June 19, President Trump took to Truth Social to announce that Apple had agreed to work with Intel to design and manufacture chips in the United States — a major win for American manufacturing, he said. Intel shares surged +10.5% to $133.82 in response, one of the stock’s best single-day gains in years. The timing is significant: Intel has been in talks with Apple for over 18 months about producing certain chips for the iPhone, MacBook, and other devices through Intel Foundry Services, as Apple looks to diversify away from its heavy reliance on TSMC. Neither Apple nor Intel has issued an official confirmation, but sources say the two companies are close to an agreement on producing lower-performance chips, with TSMC retaining the high-end work.

For SG/MY investors, the implications cut two ways. On the cautious side: if Apple shifts even a portion of its chip orders from TSMC to Intel Foundry, SG and MY suppliers in TSMC’s supply chain — particularly UMS Holdings and AEM Holdings — could face order-volume headwinds from one of their indirect key customers. On the bullish side, the broader theme of US reindustrialisation in semiconductors is accelerating demand for power, data, and packaging services globally. Keppel DC REIT and Digital Core REIT on the SGX both benefit as this manufacturing push drives data centre capacity growth. And Bursa-listed packaging names like Inari Amertron and Vitrox remain structural beneficiaries of the global chip capex supercycle regardless of which fab wins the Apple order. Watch for official confirmation from Apple and Intel — that will be the real catalyst.

4. STI Hits 5,226 New All-Time High — Why Singapore’s Index Is Asia’s Quiet Outperformer

Additionally, in a week when the hawkish Federal Reserve rattled Wall Street, Singapore’s Straits Times Index (STI) quietly hit a new all-time high of 5,226 on June 19 — breaking its own prior peak of 5,150 set just two weeks earlier on June 3. The index was up 3.32% on the week and is now 13.93% ahead year-on-year. A quarterly FTSE STI rebalance took effect on June 22, bringing fresh institutional capital into qualifying constituents. Singapore remains one of the most resilient equity markets in Asia through 2026.

The STI’s strength reflects several converging forces. First, SG banks — DBS, OCBC, UOB — which make up roughly half of the index by weight, continue to benefit from elevated net interest margins and strong dividend yields even as the rate hold introduces some uncertainty. Second, the oil price drop this week is a tailwind for Singapore Airlines, a major STI constituent, as jet-fuel costs compress. Third, Singapore’s macro fundamentals remain clean: fiscal discipline, a strong SGD, and a diversified services export base insulate the market from US rate volatility better than most EM peers. For SG/MY investors: the STI thesis is intact. DBS Group (SGX: D05) remains the core long-term holding in the index. If the Iran deal finalises and oil drops further, SIA and Capital A provide the next leg of upside. The biggest risk to watch is whether the US rate hike materialises — that could pressure SG REIT spreads and indirectly weigh on bank earnings through slower loan growth.

5. US Housing Starts Crash -15.4% in May — What It Means for SG/MY Property and REIT Investors

On the other hand, uS housing starts plunged 15.4% month-on-month in May 2026 to a seasonally adjusted annual rate of 1.177 million — the lowest level since May 2020, at the depths of the COVID shutdown. The miss against market forecasts of 1.43 million was dramatic. Multi-family starts collapsed 41.6% to 284,000, the lowest since November 2024, while single-family starts slipped 1.9% to an eight-month low of 882,000. Regionally, the South fell 17%, the West fell 17.2%, and the Northeast plunged 26.8%. The culprit is clear: mortgage rates remain stubbornly elevated, and this week’s hawkish Fed signal — which raised the probability of a December 2026 rate hike to 77% — will make construction economics even harder.

For SG/MY investors, this is primarily a risk-signal rather than a direct earnings event, but the implications are real. US-listed REITs like Manulife US REIT and Keppel Pacific Oak US REIT, which are Singapore-listed but hold US properties, face prolonged headwinds from a weak US property market and high refinancing costs. SG industrial and logistics REITs are relatively more insulated since they serve e-commerce and manufacturing demand. For Malaysian property developers — Sunway, IOI Properties, Sime Darby Property — the direct linkage to US rates is limited, but a US slowdown that deepens would weigh on MY export demand and consumer confidence. The structural risk: if the Fed does hike in late 2026, US housing could see another leg down — and that is the scenario where US-exposed REITs need active risk management.

What I’m Watching Next Week

Calendar items that could move portfolios

- Tue 23 Jun — US Consumer Confidence (Conference Board); watch for any Warsh public comments on rate outlook.

- Wed 24 Jun — Micron Technology (MU) Q3 FY2026 earnings — AI memory bellwether; consensus: $34.5B revenue (+271% YoY), ~1,000% EPS growth. Key AI capex signal.

- Thu 25 Jun — FedEx Q4 earnings (global trade proxy); US GDP Q1 final revision; Malaysia CPI May.

- Fri 26 Jun — US PCE inflation May (the Fed’s preferred gauge — critical given hawkish dot plot); Singapore industrial production May.

- All week — US-Iran Geneva talks resumption status; Brent crude tape; any Intel/Apple official statement on the chip deal.

Bottom Line

This week gave SG/MY investors a lot to process. The fed rate hike 2026 signal is real — the dot plot does not lie, and 77% futures pricing confirms it. At the same time, the oil peace dividend is materialising faster than most expected, and that is an enormous structural tailwind for Singapore Airlines, AirAsia, and import-heavy Malaysian consumers. The Intel-Apple deal and the STI’s new all-time high are reminders that individual corporate catalysts and domestic macro strength can coexist with a hawkish Fed. The practical playbook: hold your USD T-bill ladder at 4%+, stay patient on SG REITs, watch the Iran deal for the oil rotation signal, and keep Micron’s earnings on June 24 in your diary as the next AI capex data point. Stay curious, do your own research, and remember — every big market week creates the opportunities that disciplined investors harvest over the following months.

For educational purposes only. Not financial advice. Always do your own research. Catch up on last week’s issue: GoodWhale Weekly: Nvidia $81.6B Record Quarter, SpaceX IPO, Iran Oil at $87.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

[…] Previous […]