The Week in 30 Seconds

- [OIL/GEO] Oil surges Iran strikes. Brent topped $76, WTI held above $72, up ~5% on the week after the US struck Iran and Iran hit back at US Gulf infrastructure. Oil-sale waiver expires July 17.

- [TECH/IPO] SK Hynix’s record IPO. Raised $26.5B in the biggest-ever foreign US listing, stock closed its debut day up 13%, demand ran 7x the shares on offer.

- [MACRO] Fed split 9-8 on hikes. June minutes showed a deeply divided committee under new Chair Warsh. He testifies before Congress Tuesday alongside June’s CPI print.

- [EARNINGS] Delta beats to open earnings season. Adjusted EPS $1.56 vs $1.48 estimate, record revenue despite record fuel costs, dividend raised 15%.

- [EARNINGS] PepsiCo: US soft, Asia strong. Revenue beat, EPS narrowly missed. US beverage volumes fell 4%, but Asia Pacific and international volumes grew.

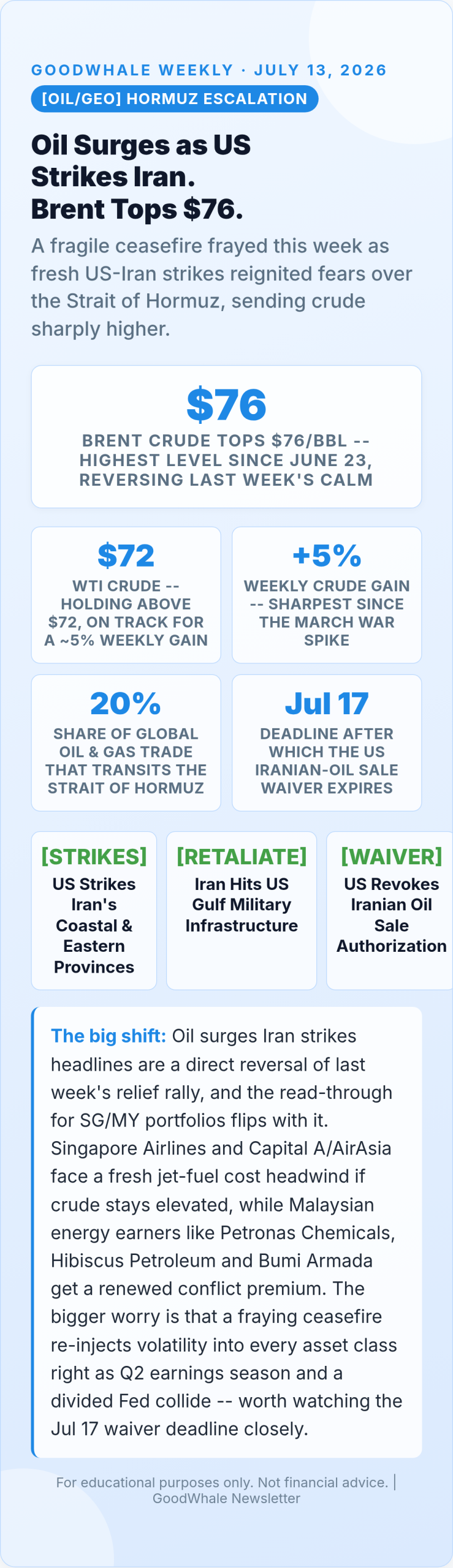

1. Oil surges Iran strikes: Oil Surges Iran Strikes: Brent Tops $76 as Hormuz Ceasefire Frays

Meanwhile, just a week after crude looked like it had round-tripped back to pre-war levels, the calm didn’t last. Oil surges Iran strikes headlines dominated the week after Washington struck Iran’s southern coastal and eastern provinces, prompting Tehran to retaliate with attacks on US military infrastructure in Gulf states on Thursday. Brent crude jumped above $76 a barrel, its highest level since June 23, while WTI held above $72 and was on pace for a weekly gain of nearly 5% — the sharpest weekly move since the original war spike in March. The renewed hostilities strain a ceasefire that Washington and Tehran had signed barely a month earlier to end their nearly four-month conflict.

The mechanics matter for anyone tracking energy markets: roughly 20% of global oil and gas trade transits the Strait of Hormuz, and shipping through the strait remains significantly disrupted as tanker traffic struggles to normalise around the renewed strikes. Adding urgency, the US Treasury’s temporary authorization for Iranian oil sales expires just after midnight on July 17, meaning the market has a hard deadline to watch for the next leg of this story. Energy analysts now expect prices to stay elevated as hazardous conditions persist and emergency stockpile releases wind down. For SG/MY investors, the flip from last week’s oil-steadying narrative to this week’s oil surges Iran strikes headlines is a reminder that geopolitical premiums can reverse fast — Singapore Airlines and AirAsia face renewed jet-fuel pressure, while Malaysian energy names such as Petronas Chemicals and Hibiscus Petroleum stand to benefit from the higher price deck.

| Benchmark | This Week | Last Week | Weekly Move |

|---|---|---|---|

| Brent Crude | $76 | $71-72 | +5-6% |

| WTI Crude | $72 | $69 | +~5% |

| Hormuz Flows | Disrupted | 10M+ bpd | Reversed |

| US-Iran Status | Renewed Strikes | Ceasefire Holding | Deteriorated |

2. SK Hynix’s Record $26.5B IPO: Biggest Foreign Listing in US History

Notably, while oil grabbed the geopolitical headlines, the biggest pure market story of the week came out of Nasdaq. SK Hynix raised $26.5 billion in its US debut on Friday July 10, the largest-ever first-time listing by a foreign company on a US exchange, eclipsing Alibaba’s $25 billion IPO in 2014. The South Korean memory chip leader priced its American depositary receipts at $149 each — a 3% premium to its Korean close — and the offering of 177.9 million ADRs (representing 17.79 million underlying shares) drew investor demand running at seven times the available shares. The stock opened around $170 and closed its first session up roughly 13% at $168, pushing SK Hynix’s market value past $1.27 trillion.

The company said all proceeds will fund two capacity expansion projects: its Yongin fab in South Korea and a new US packaging facility, both aimed squarely at meeting high-bandwidth memory (HBM) demand for AI infrastructure. SK Hynix’s chairman told CNBC that “demand is enormous” — a pointed contrast to last week’s chip stock selloff, when reports of a slower SK Hynix HBM expansion pace had spooked Micron and Sandisk. Regular trading under the ticker SKHY begins this Monday. For SG/MY portfolios, the read-through is bullish: UMS Holdings, AEM Holdings, Frencken Group, Inari Amertron and Vitrox are the region’s picks-and-shovels names most exposed to SK Hynix’s expansion, and a 7x-oversubscribed mega-IPO is a strong vote of confidence that AI-driven memory demand has staying power into 2027.

3. Fed Split 9-8 on Rate Hikes: Warsh’s First Minutes Reveal a Divided Committee

However, the minutes from Fed Chair Kevin Warsh’s first meeting at the helm, released Wednesday July 8, showed a Federal Open Market Committee genuinely torn over where rates go next. Of the 18 policymakers who submitted 2026 rate projections after the June 16-17 meeting, the committee split roughly 9-8 on whether rates should rise this year, with six officials going so far as to back two full quarter-point hikes. A few officials argued there was an active case for raising rates at the June meeting itself due to sticky inflation, even though the committee ultimately voted unanimously to hold rates steady. Others saw a path where cooling inflation would allow cuts later this year — the kind of genuine two-sided debate that hadn’t been on public display under the previous Fed leadership.

The minutes matter less for what already happened and more for what’s coming: Warsh testifies before Congress this Tuesday, July 14, the same day June’s CPI report lands — a combination that could move markets sharply in either direction depending on how hawkish or dovish his tone lands. The next actual rate decision doesn’t come until the July 28-29 FOMC meeting, leaving nearly three weeks of data-watching in between. For SG/MY investors, an evenly split Fed under a new chair is inherently harder to trade around than a committee with a clear consensus — MAS’s own policy stance on the S$NEER, and the direction of SGD and MYR, will likely take cues from how Tuesday’s CPI print and Warsh’s testimony shift the rate-hike odds market.

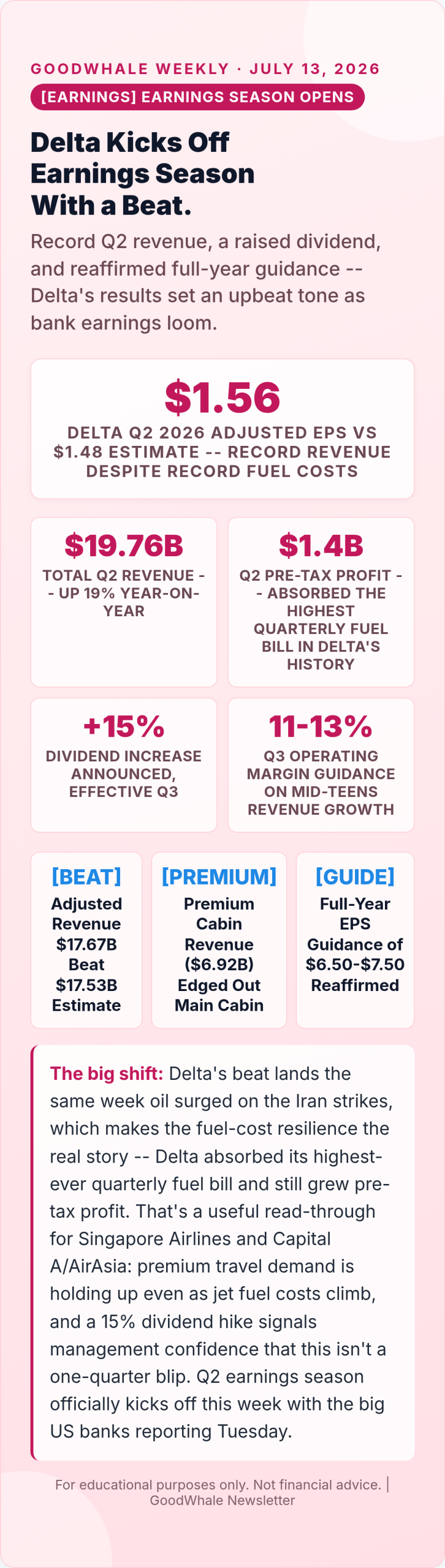

4. Delta Earnings Kick Off Q2 Season: Record Revenue Beats Fuel Cost Headwinds

Additionally, delta Air Lines opened the Q2 2026 earnings season on a strong note, reporting Friday July 10. Adjusted EPS came in at $1.56 versus the $1.48 analysts expected, on adjusted revenue of $17.67 billion that cleared the $17.53 billion estimate. Total reported revenue hit $19.76 billion, a 19% jump from $16.65 billion a year earlier — notably, that gain came almost entirely from higher fares and a richer mix rather than flying more planes, with capacity up only about 1% while adjusted revenue climbed roughly 14%. Premium cabin revenue reached $6.92 billion, narrowly outpacing the main cabin’s $6.85 billion, underscoring how much of the airline’s growth is coming from travelers trading up.

The standout detail is that Delta delivered $1.4 billion in pre-tax profit while absorbing the highest quarterly fuel expense in company history — a direct real-world test of exactly the kind of oil-price pressure this week’s Iran-strikes story is putting back on the table. Management responded with confidence, not caution: a 15% dividend increase takes effect in Q3, and the company reaffirmed its full-year guidance of $6.50 to $7.50 adjusted EPS and $3-4 billion in free cash flow, while guiding Q3 operating margin to 11-13% on mid-teens revenue growth. For SG/MY investors, Delta’s results are an encouraging early data point for Singapore Airlines and Capital A/AirAsia heading into their own reporting seasons — premium travel demand is proving resilient even as fuel costs climb, though the bigger test for the sector arrives if this week’s oil spike proves durable rather than a spike-and-fade.

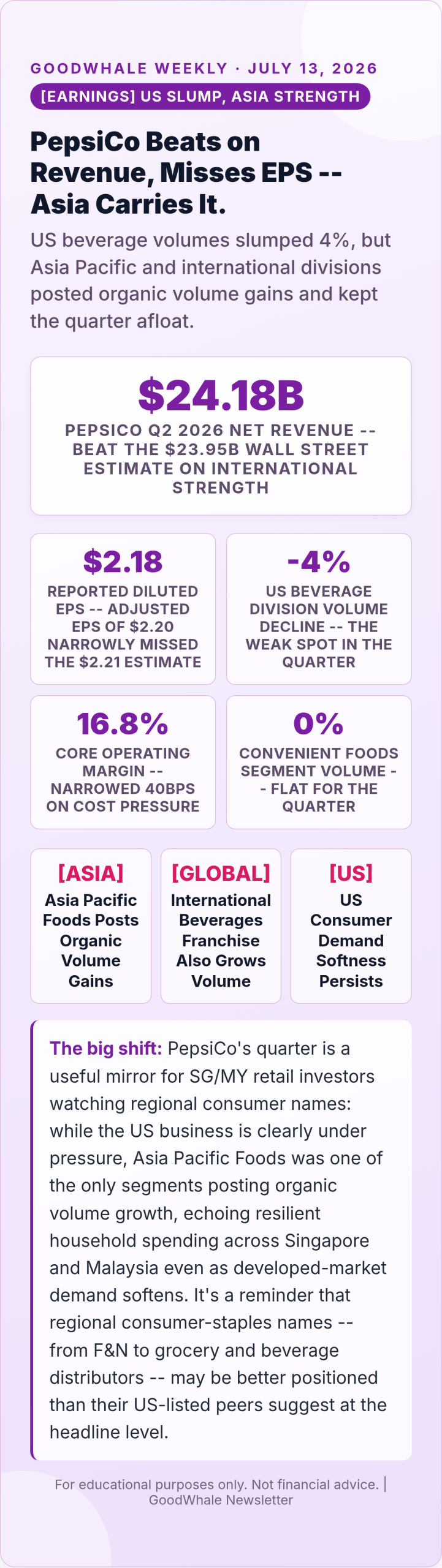

5. PepsiCo Q2 2026: Asia Pacific Volume Growth Offsets a Soft US Quarter

On the other hand, pepsiCo’s second-quarter report, out Thursday July 9, was a study in geographic divergence. Net revenue of $24.18 billion topped the $23.95 billion Wall Street target, a 6.4% year-on-year increase, while diluted EPS of $2.18 came in below the adjusted $2.20 figure the Street was modeling at $2.21 — a narrow miss that sent shares lower premarket. Operating profit rose to $4.02 billion and net income attributable to PepsiCo reached $2.98 billion, but core operating margin narrowed 40 basis points to 16.8% as cost pressures partially offset pricing and productivity gains.

The real story was underneath the headline numbers: PepsiCo’s US beverages unit suffered a 4% volume drop and the convenient foods segment was flat, but overseas divisions — including Asia Pacific Foods and the International Beverages Franchise — all recorded organic volume gains, making international operations the company’s clearest source of momentum this quarter. Management reaffirmed full-year guidance but flagged that results may land toward the lower end of the EPS range. For SG/MY investors, the Asia Pacific volume strength inside a US giant’s earnings report is a small but telling data point: it suggests regional consumer demand is holding up better than in the US, which should be read as a modestly encouraging signal for locally listed consumer-staples and F&B names navigating the same cost pressures PepsiCo describes globally.

What I’m Watching Next Week

Key data and events — July 14 to July 17

- Tue 14 Jul — June CPI report and Fed Chair Warsh’s Congressional testimony land the same day; JPMorgan, Bank of America, Goldman Sachs, Wells Fargo and Citigroup all report Q2 earnings.

- Wed 15 Jul — June PPI and the Fed’s Beige Book; ASML, Johnson & Johnson, Morgan Stanley, BlackRock and United Airlines report.

- Thu 16 Jul — Taiwan Semiconductor, Netflix, UnitedHealth and GE Aerospace headline a heavy earnings day; watch TSMC commentary for read-through on the SK Hynix-driven AI memory story.

- Fri 17 Jul — The US Treasury’s Iranian oil-sale waiver expires just after midnight — a hard deadline for the next leg of the Strait of Hormuz story.

- All week — Watch for follow-through on SK Hynix’s SKHY ticker in regular trading and whether regional supply-chain names (AEM, UMS, Frencken, Inari, Vitrox) catch a bid.

Bottom Line

Five stories, two big surprises. Oil surges Iran strikes reversed last week’s calm in a matter of days — a reminder that geopolitical ceasefires can be fragile, and that Singapore Airlines, Capital A/AirAsia and Malaysian energy earners are on opposite sides of the same trade. SK Hynix’s record-breaking IPO is the strongest possible rebuttal to last week’s chip-selloff jitters: a 7x-oversubscribed, $26.5 billion raise says AI memory demand is not going anywhere, and it’s a genuine tailwind for the region’s HBM supply chain. The Fed’s 9-8 split under a brand-new chair means Tuesday’s CPI print and Warsh’s testimony carry outsized weight for where SGD, MYR and rate-sensitive REITs go next. And on earnings, Delta’s fuel-cost resilience and PepsiCo’s Asia Pacific strength both point the same direction: demand is holding up better than headline noise would suggest, even as costs climb. Practical playbook: watch the July 17 oil-waiver deadline, keep an eye on SKHY’s first week of regular trading, and treat Tuesday’s CPI-plus-Warsh combination as the single most important catalyst of the week ahead.

For educational purposes only. Not financial advice. Always do your own research. Catch up on last week’s issue: GoodWhale Weekly: Chip Stock Selloff 2026, Jobs Shock Cools the Fed, Nike’s Soft China Quarter.

Source: oil prices surge as renewed Iran strikes rattle the Strait of Hormuz

{kind=link}

{kind=link}

{kind=link}

{kind=link}

[…] Previous […]