The Week in 30 Seconds

- 📌 Nvidia $81.6B quarter. Up 85% YoY. Q2 guided to $91B. Blackwell chips backordered globally. Data centre +92% YoY.

- 🏢 Warsh takes the Fed. Sworn in as chair. PCE at 3.3%, wholesale prices +6% YoY. Rate hike now likelier than a cut in 2026.

- 🚀 SpaceX S-1 filed. OpenAI targets September confidential filing. $3.7T AI IPO pipeline — retail will get scraps at best.

- 🤝 Trump-Xi Beijing summit. $17B agri deals + 200 Boeing jets agreed. No signed tariff deal; KLCI dipped on the ambiguity.

- 🛢 Iran & $87 Brent. 20% of global oil through Hormuz stays at risk. PCE 3.3% = zero rate cut probability for 2026.

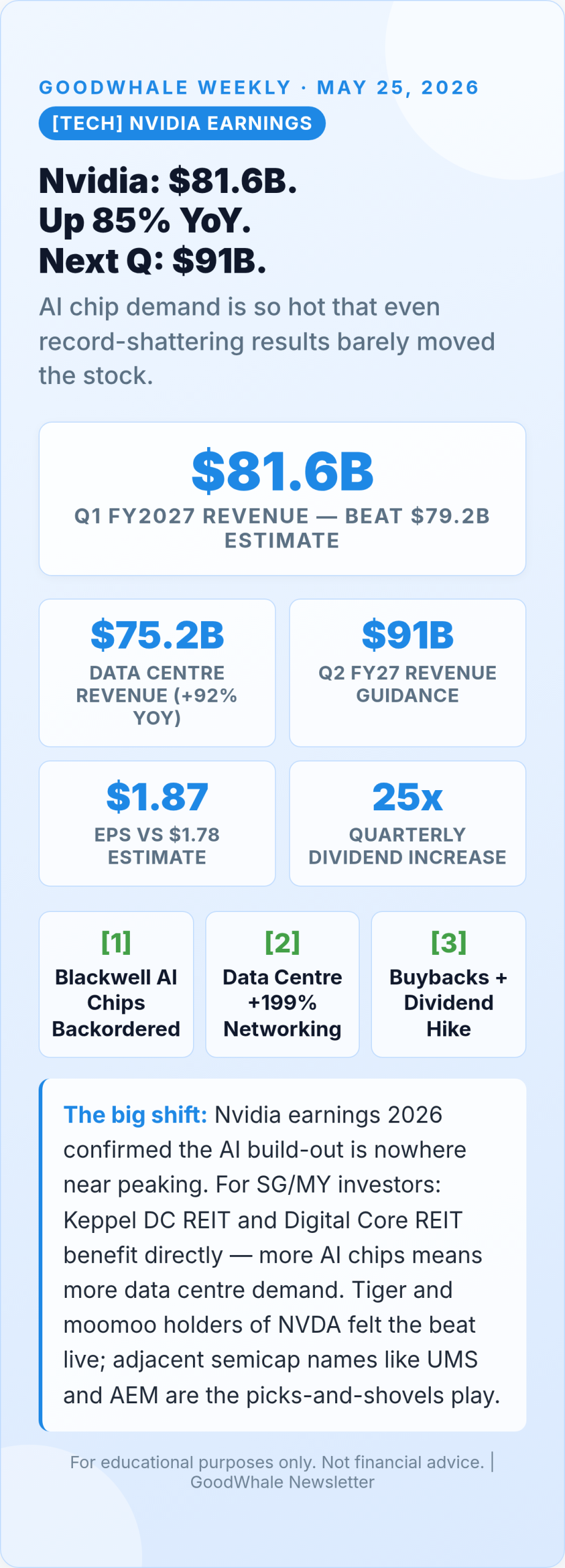

1. Nvidia earnings 2026: Nvidia Posts $81.6B in One Quarter — AI Chip Demand Still Going Vertical

Meanwhile, nvidia’s Q1 FY2027 earnings landed Wednesday May 21 and were, in a word, staggering. Revenue hit $81.6B, beating the $79.2B Wall Street estimate, and up an eye-watering 85% year-on-year. Data Centre revenue alone clocked $75.2B — a 92% YoY jump — driven almost entirely by the insatiable demand for Blackwell AI chips that are still backordered globally.

What makes this nvidia earnings 2026 print different from prior quarters is the guidance: CEO Jensen Huang guided Q2 FY27 to $91B, implying the growth trajectory is not slowing. EPS came in at $1.87 versus the $1.78 estimate, and the company announced a 25-times increase in its quarterly dividend — a signal of extreme balance-sheet confidence. Networking revenue surged +199% YoY as the AI infrastructure stack broadens beyond pure compute. For SG/MY retail investors: if you hold Keppel DC REIT, Digital Core REIT, or Mapletree Industrial Trust, you own a slice of the physical infrastructure that makes this compute explosion possible.

| Nvidia Quarter | Revenue | YoY Growth | Data Centre |

|---|---|---|---|

| Q1 FY2027 (May 2026) | $81.6B | +85% | $75.2B |

| Q4 FY2026 (Feb 2026) | ~$70B | +78% | ~$64B |

| Q1 FY2026 (May 2025) | $44.1B | +69% | $39.1B |

| Q1 FY2025 (May 2024) | $26.0B | +262% | $22.6B |

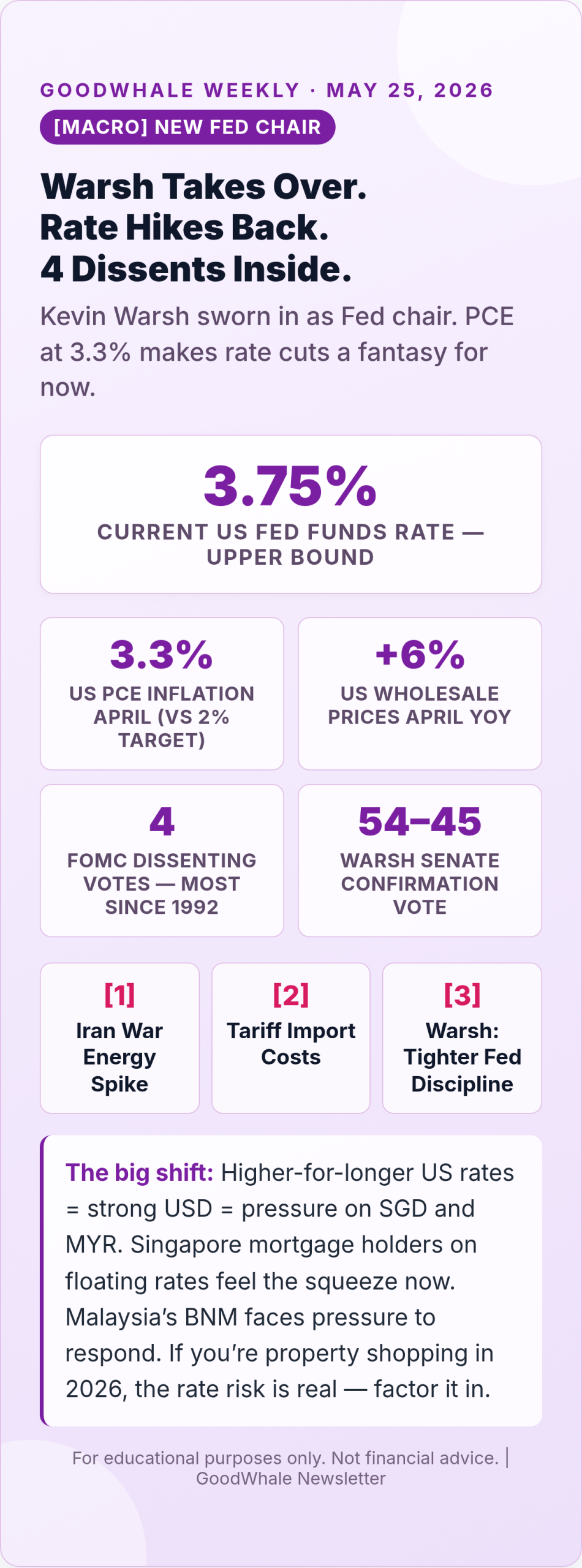

2. Kevin Warsh Sworn In as Fed Chair — Rate Hike Now Likelier Than a Cut

Notably, the Federal Reserve has a new boss. Kevin Warsh was confirmed 54–45 by the Senate and sworn in this past week, making him the first Fed chair since the 1990s to take office with four dissenting FOMC votes on his first day. The hot backdrop: US PCE inflation estimate for April came in at 3.3%, well above the 2% target, while wholesale prices surged +6% year-on-year. CME FedWatch now shows zero probability of a 2026 rate cut — in fact, a hike has entered the conversation.

Warsh’s stated philosophy is tighter discipline and leaner Fed communications — less forward guidance, more data dependence. The macro drivers are entrenched: energy prices bid up by the Iran-Hormuz conflict, tariff pass-through keeping import costs elevated, and a labour market that refuses to crack. For SG/MY investors, the playbook is: strong USD headwind on EM equities and REITs. Hold USD T-bills at 4%+ while the cut narrative stays dead. Singapore bank stocks (DBS, OCBC, UOB) have mixed signals — higher short rates crimp NIMs but credit demand holds. Property buyers on floating-rate mortgages in both SG and MY: model for 3.75–4.0% funds rate through at least mid-2027.

3. SpaceX Files S-1, OpenAI Eyes September — A $3.7T AI IPO Wave Is Coming

However, two of the most transformative companies in modern history are heading for public markets in the same window. SpaceX filed its S-1 prospectus on May 20, making its audited financials public for the first time ever. The implied valuation hovers around $1 trillion, partly reflecting a potential merger with Elon Musk’s xAI. OpenAI, meanwhile, is targeting a confidential S-1 filing by September 2026 at a similar ~$1T valuation. Add Anthropic (maker of Claude, reportedly not far behind), and you have a $3.7T pipeline of AI-native companies hitting public markets within months of each other.

For SG/MY retail investors, the honest answer is: you will not get IPO allocation. Institutions lock up the opening shares; retail buys into secondary market frenzy, often at inflated prices. The smarter approach: build exposure to the supply chain now. TSMC supplies the chips for all three. Keppel DC REIT, Digital Core REIT, and Mapletree Industrial Trust on the SGX provide data centre exposure that grows regardless of which AI company wins. If you want listed AI exposure today, consider the CSOP USD Money Market ETF as a cash alternative while you wait for post-IPO price discovery to settle.

4. Trump Flew to Beijing, Got $17B in Deals — But Markets Want a Tariff Agreement

Additionally, president Trump’s Beijing visit this past week produced tangible wins: China committed to $17B in annual US agricultural purchases through 2028 (soybeans, corn, wheat), agreed to buy 200 Boeing aircraft, and the two sides established two new institutions — a Board of Trade and a Board of Investment. A tariff reduction framework covering $30B+ in goods was also discussed, with the next Trump-Xi meeting slated for September 2026 on US soil.

But Asian markets, including the KLCI, dipped on the lack of a signed tariff deal. “Framework discussed” is not the same as “tariffs reduced.” The question for SG/MY investors is timing: if a binding deal materialises in September, the relief rally in trade-exposed names would be significant. Singapore sits in a sweet spot as a neutral logistics and financial hub — every uptick in US-China trade flows through SGX-listed port and logistics names. Malaysia recorded record April exports and would see further upside through Petronas Chemicals and tech supply-chain names like Inari Amertron and Vitrox on the Bursa.

5. Iran Conflict Keeps Brent at $87 — And Takes Rate Cuts Completely Off the Table

On the other hand, the Iran-US conflict is now the single most important macro variable for global inflation — and most retail investors aren’t pricing it correctly. Brent crude at $87/barrel reflects a persistent risk premium on Strait of Hormuz disruption, through which 20% of global oil supply passes. US PCE inflation (the Fed’s preferred gauge) is estimated at 3.3% for April, wholesale prices are up +6% year-on-year, and CME FedWatch shows a zero probability of a 2026 Fed rate cut. A hike is now live in the pricing.

The SG/MY split is clear. Malaysia wins: Petronas upstream revenues rise with every dollar Brent climbs above $75. Government oil revenues that fund the national budget improve. Listed plays: Hibiscus Petroleum, Bumi Armada, Sapura Energy. Singapore feels the pain: as an importer of virtually all energy, petrol prices, electricity tariffs, and the prices of every manufactured good that travels in a ship using fuel are all moving higher. MAS has already tightened its S$NEER slope. For both markets, the Iran situation is not a short-term blip — it is the structural backdrop for the next 12-24 months of portfolio positioning.

What I’m Watching Next Week

Calendar items that could move portfolios

- Mon 26 May — US Memorial Day (markets closed). Good day to review your portfolio allocation.

- Tue 27 May — US Consumer Confidence (May); Singapore Q1 GDP final revision; BNM Malaysia rate watch.

- Wed 28 May — US GDP Q1 second revision; Singapore May manufacturing PMI; Trump-Xi trade deal follow-up headlines.

- Thu 29 May — US PCE inflation April final — the Fed’s most-watched gauge. Consensus 3.3%. Any surprise moves markets hard.

- Fri 30 May — US Core PCE; Personal income & spending; month-end institutional rebalancing flows.

- All week — Iran-Hormuz headlines; Warsh’s first Fed communications as chair; SpaceX S-1 analyst coverage launches.

Bottom Line

Five stories, one thread: the AI build-out is accelerating (Nvidia earnings 2026 proved it), the macro environment is hawkish (Warsh, PCE 3.3%, zero rate cut odds), geopolitics is the wild card (Iran at $87 Brent, Trump-Xi without a deal), and the next generation of public AI companies is about to arrive (SpaceX, OpenAI). For a SG/MY retail investor in May 2026, the question is not which hot stock to chase — it is whether your portfolio is built to survive higher-for-longer rates, sustained energy inflation, and a USD that stays bid. Quality compounders, data centre REITs, upstream Malaysia energy names, and a USD T-bill ladder at 4%+ is how I would play it heading into June.

For educational purposes only. Not financial advice. Always do your own research. Catch up on last week’s issue: GoodWhale Weekly: Warsh Takes the Fed, CPI Hot at 3.8%, Cisco’s Dot-Com Pop.

Source: Nvidia investor relations

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply