The Week in 30 Seconds

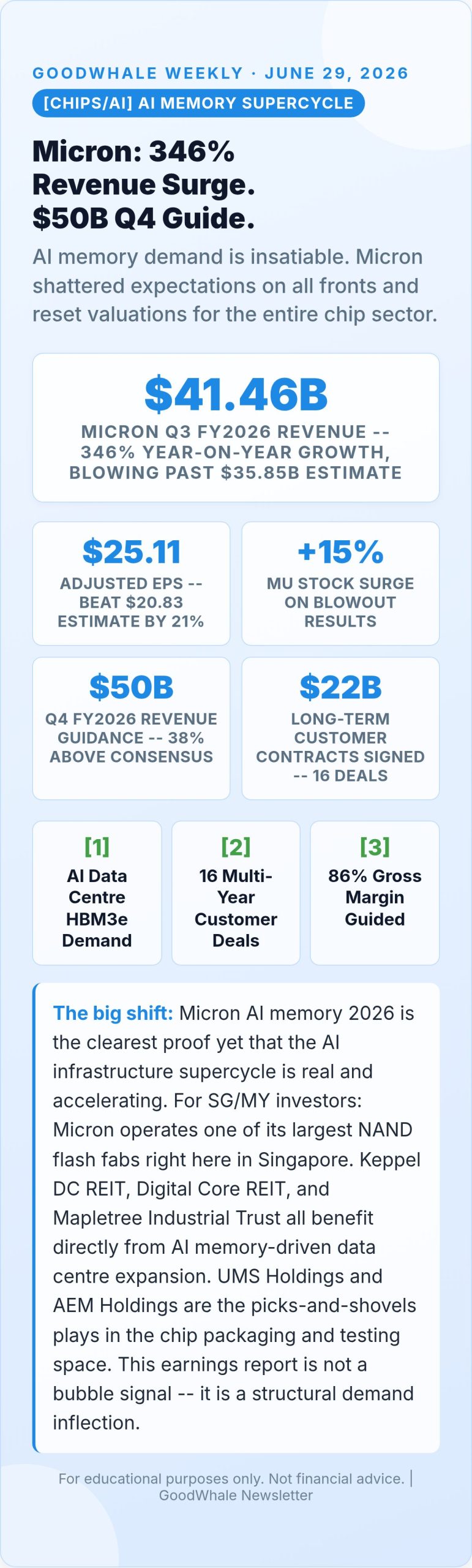

- [CHIPS/AI] Micron AI memory 2026 blowout. Revenue $41.46B (+346% YoY), EPS $25.11 vs $20.83 est, stock +15%. Q4 guide: $50B. $22B in multi-year customer contracts. AI memory supercycle confirmed.

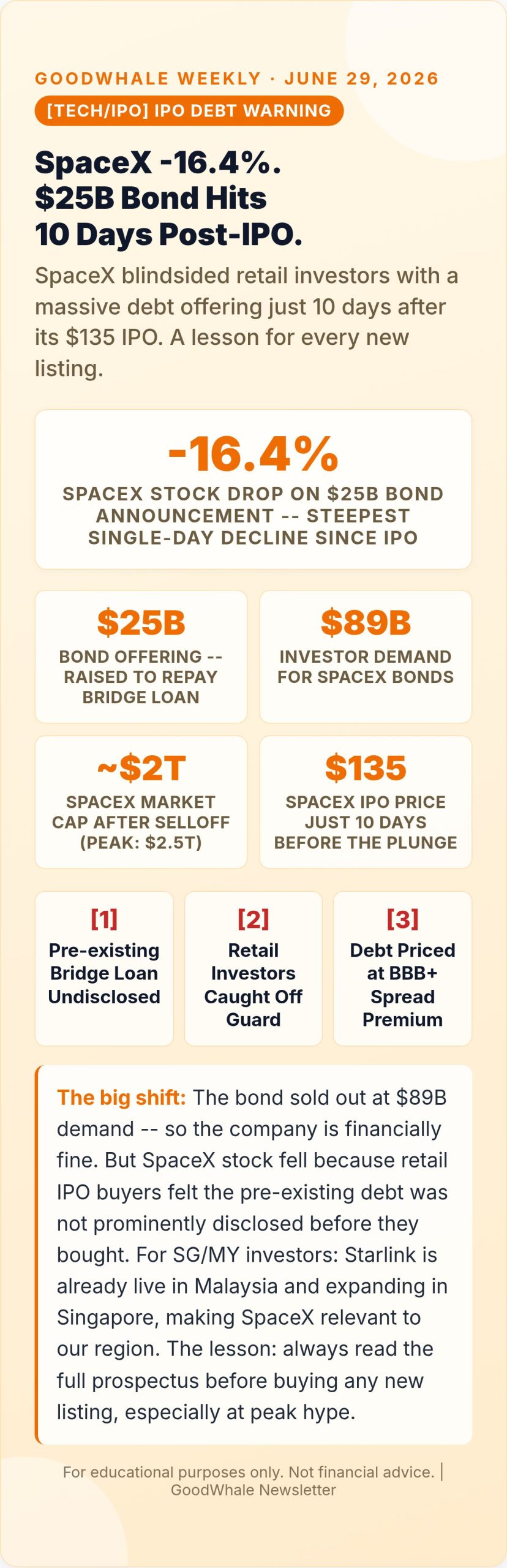

- [TECH/IPO] SpaceX bond shock. Stock fell 16.4% just 10 days after the $135 IPO on a $25B bond offering. Bonds drew $89B demand — the company is fine. Retail IPO buyers got a prospectus lesson.

- [OIL/GEO] Oil hits post-war lows. WTI at $81.38, Brent at $84.21 — lowest since before the US-Iran war. $30+ geopolitical premium evaporating. MY energy names under pressure; SIA/AirAsia are winners.

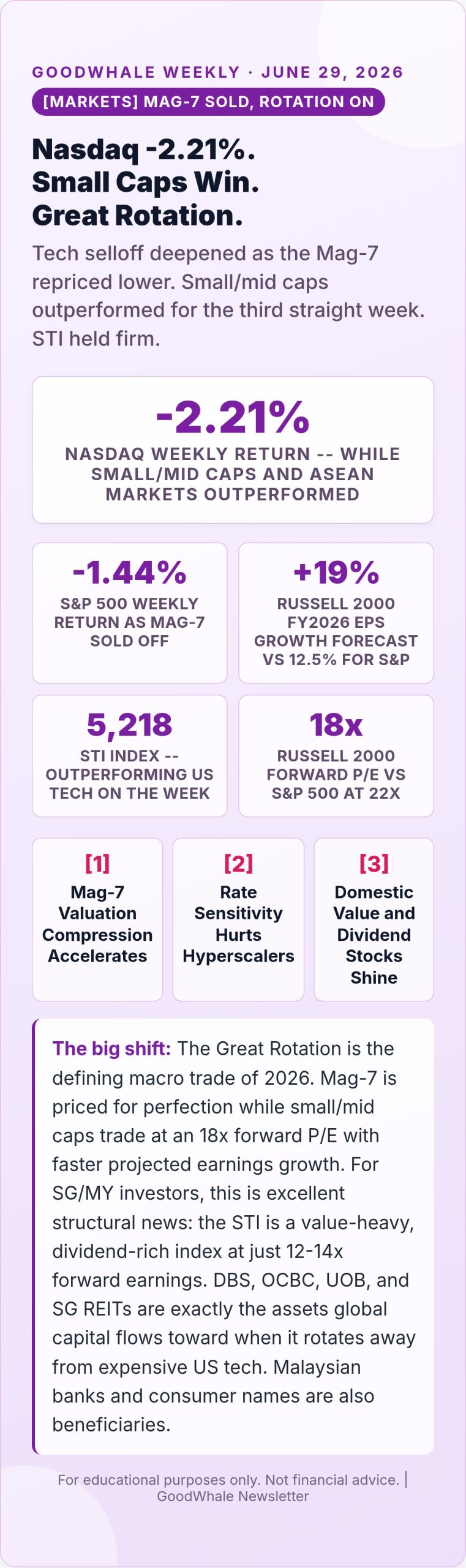

- [MARKETS] Great Rotation deepens. Nasdaq -2.21%, S&P -1.44% as Mag-7 sold off. Small/mid caps outperformed. STI held at 5,218. Russell 2000 forward P/E at 18x vs S&P 22x — value wins.

- [AI/DATA] AI margin squeeze emerges. Databricks +80% revenue but margins shrinking. Cerebras -10% on margin warning. Picks-and-shovels (Micron, DC REITs, chip packagers) confirmed as the smarter AI trade.

1. Micron AI memory 2026: Micron AI Memory 2026: $41B Revenue, 346% YoY — The AI Memory Supercycle Is Undeniable

Meanwhile, micron Technology reported Q3 FY2026 results on June 24 that left Wall Street speechless. Revenue came in at $41.46 billion — against a consensus estimate of $35.85 billion — representing a staggering 346% year-on-year surge from just $9.30 billion a year earlier. Adjusted EPS hit $25.11, crushing the $20.83 estimate by 21%. The headline driver: insatiable AI data centre demand for High Bandwidth Memory (HBM) and NAND flash storage. Micron’s Cloud Memory Business Unit alone reported $13.77 billion in Q3 revenue at an 83% gross margin. The company also announced 16 long-term customer agreements — spanning data centres, hyperscalers, and automakers — covering multi-year periods and committing an estimated $22 billion in future financial obligations. This is Micron AI memory 2026 firing on all cylinders. The stock closed up +15% the following day, lifting the entire semiconductor sector.

Forward guidance was equally stunning: Micron guided for $50 billion in Q4 FY2026 revenue with an 86% gross margin — well ahead of the $43.2 billion consensus estimate. For SG/MY investors, the playbook is clear. Micron operates one of the world’s largest NAND fab sites in Singapore, making the city-state a direct beneficiary of the AI memory supercycle through manufacturing employment, industrial land demand, and supply-chain activity. Keppel DC REIT (SGX: AJBU) and Digital Core REIT (SGX: DCRU) benefit as AI memory growth drives insatiable data centre capacity demand across the region. In Malaysia, Inari Amertron and Vitrox are semiconductor packaging and testing plays positioned to capture chip capex overflow. The key risk: a demand cliff if AI model training plateaus. But with 16 multi-year contracts locked in, Micron’s revenue visibility is as strong as it has ever been.

| Quarter | Revenue | Adj. EPS | YoY Revenue Growth |

|---|---|---|---|

| Q3 FY2026 (reported Jun 24) | $41.46B | $25.11 | +346% |

| Q2 FY2026 (Mar 2026) | ~$28B | ~$17 | ~+220% |

| Q3 FY2025 (Jun 2025) | $9.30B | $1.79 | Baseline |

| Q4 FY2026 Guide | ~$50B | ~$30 est. | +437% est. |

2. SpaceX -16.4% After $25B Bond Shock — What SG/MY IPO Investors Must Learn from This

Notably, on June 23, SpaceX announced a $25 billion bond offering — just ten days after listing on the public markets at $135 per share. The announcement triggered the stock’s steepest single-day decline since its debut, down 16.4%. At its post-IPO peak, SpaceX carried a market capitalisation above $2.5 trillion, briefly overtaking Alphabet. After the selloff, it sat just above $2 trillion. The bond itself was a commercial success: demand hit $89 billion on a $25 billion deal, and bonds were priced across five tranches from 2031 to 2056. SpaceX stated the proceeds would repay an existing bridge loan facility and fund general corporate purposes. The problem was the optics: a $25 billion pre-existing debt obligation was embedded in the company before retail investors bought a single share, and the bond was announced before the ink was dry on many investor purchase confirmations.

For SG/MY investors, this is a masterclass in new listing risk. SpaceX is genuinely extraordinary — Starlink is already commercially live in Malaysia and in approved rollout for Singapore business users, making it one of the most ASEAN-relevant US companies on any exchange. But the stock mechanics of a fresh listing — lock-up expirations, undisclosed debt structures, insider selling windows — create short-term volatility that can trap retail buyers at the wrong entry point. The rule of thumb: read the full prospectus, not just the roadshow deck. Understand the capital structure before you chase the hype. SpaceX will likely recover as Starlink revenue grows globally, but the investors who bought at peak enthusiasm on IPO day and held through the -16.4% drop were given an expensive reminder. Long-term the business is extraordinary. The entry price and debt load always matter.

3. Oil Hits Post-War Lows on Iran Deal Progress — The SG/MY Energy Rotation Trade You Need to Know

However, on June 24, global oil prices fell to their lowest level since before the US-Iran war. WTI crude settled at $81.38 per barrel — down more than 4% on the week — while Brent fell 3.6% to $84.21. The catalyst: US and Iranian officials confirmed their peace framework was advancing, with Iran sanctions relief taking effect immediately upon formal ratification and a commitment to reopen the Strait of Hormuz — the maritime chokepoint through which approximately 20% of the world’s oil and LNG passes daily. Before the war, a supply shock triggered by Hormuz disruptions had baked an estimated $30+ per barrel geopolitical premium into crude prices. That premium is now evaporating fast. The direction is clear even though the deal is not yet officially signed.

For SG/MY investors, the oil drop creates a sharp rotation trade. On the bearish side for Malaysia: energy names that rode the conflict premium — Hibiscus Petroleum, Bumi Armada, and Petronas Chemicals — face direct earnings headwinds. Malaysia’s national oil company Petronas, which funds a significant portion of the federal budget, also sees reduced dividend capacity at lower crude. On the bullish side for Singapore: Singapore Airlines (SIA) and Capital A / AirAsia are the clearest winners — jet fuel represents their largest operating cost, and lower Brent directly expands margins. Lower oil is also globally disinflationary: if it holds, it gives the US Federal Reserve a data-driven argument to pause its hawkish stance, which would be a powerful catalyst for SG REITs whose valuations are suppressed by elevated rates. The risk to this trade: the Iran deal is not yet fully finalised. Monitor the tape on any Geneva talks update.

4. Nasdaq -2.21% as Great Rotation Picks Up Steam — SG/MY Investors Are in the Right Place

Additionally, the week of June 23 saw US technology stocks come under sustained pressure. The Nasdaq Composite fell 2.21% while the S&P 500 dropped 1.44%, as the Magnificent 7 — Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, and Tesla — led declines on a combination of valuation pressure, hawkish Fed overhang, and investor rotation. At the same time, small and microcap stocks outperformed large caps, extending a trend that has been building across 2026. The Russell 2000 small-cap index is on track for 19% earnings growth in 2026 versus a 12.5% forecast for the S&P 500, yet trades at just 18x forward earnings compared to the S&P 500’s 22x+. Meanwhile, Singapore’s STI held at 5,218 — outperforming US tech meaningfully on the week, reinforcing its position as one of Asia’s most resilient markets through 2026.

The Great Rotation thesis is simple: after years of Mag-7 dominance, capital is flowing toward cheaper, more domestic-focused businesses. For SG/MY retail investors, this structural shift is home advantage. The STI is inherently a value-and-dividend market. DBS Group (SGX: D05), OCBC, and UOB — which together dominate the index — pay dividend yields of 5-7% and trade at attractive book-value multiples relative to US bank peers. SG industrial and logistics REITs like Mapletree Logistics Trust and AIMS APAC REIT offer income characteristics that global capital is rediscovering as the tech premium compresses. In Malaysia, Maybank, CIMB Group, and Public Bank also represent the kind of steady-compounding value that benefits from a rotation out of growth. The watch item: the June 27 Russell reconstitution, where the fastest-growing small caps will graduate to the Russell 1000 — watch for the flows as index trackers rebalance into the new constituents on Monday June 30.

5. Databricks +80% Revenue but Margins Shrinking — Why SG/MY Investors Should Own AI Infrastructure, Not Apps

On the other hand, the week produced a clear AI two-speed story. On Tuesday June 23, Databricks — the data and AI infrastructure company — reported sales growth topping 80% year-on-year for fiscal 2026. The revenue surge is unambiguous proof that enterprise AI adoption is accelerating. But the bottom line told a more complex story: margins are shrinking as the cost of running AI agents — the compute, GPU time, and orchestration infrastructure they require — rises faster than the revenue they generate. On Wednesday June 24, Cerebras Systems — the AI chip maker that went public this year — fell 10% after its debut earnings report forecast further margin compression in coming quarters. Neither company is failing; both are growing fast. But profitability is being deferred as AI agent costs run ahead of monetisation.

For SG/MY investors, this split gives an important portfolio signal. AI application layer plays — software companies building AI products — are delivering revenue but facing margin pressure that will take quarters to resolve. AI infrastructure plays — the memory, compute, and data centre capacity that AI runs on — are collecting the revenue regardless of which AI application wins. Micron’s blowout earnings this week are the best illustration: Micron does not care whether Databricks or a competitor wins the enterprise AI market. Every AI agent runs on HBM memory and NAND storage. For SGX-listed picks-and-shovels: Keppel DC REIT (data centres), Digital Core REIT (hyperscale data centres), and Mapletree Industrial Trust (hi-tech facilities) are the Singapore infrastructure plays. In Malaysia, Inari Amertron and Vitrox are the semiconductor testing and packaging names exposed to the AI chip capex cycle. The strategy: let the software companies fight for margin share. Own the pick, not the miner.

What I’m Watching Next Week

Half-year wrap and key data releases — June 30 to July 4

- Mon 30 Jun — Russell reconstitution in effect: index rebalance flows hit as new Russell 1000/2000 constituents are purchased. Also: Japan Tankan survey; SG industrial production May final.

- Tue 1 Jul — US ISM Manufacturing PMI June (key read on industrial health); China Caixin Manufacturing PMI; KLCI half-year performance wrap. Watch for any DBS or OCBC ex-dividend date effects.

- Wed 2 Jul — US ADP private payrolls (jobs preview); Malaysia trade balance May; any update on Iran deal finalisation from Geneva.

- Thu 3 Jul — US markets close early (pre-July 4 holiday); US initial jobless claims; Fed meeting minutes (if any). Last full Asia trading day of the week.

- Fri 4 Jul — US Independence Day — markets closed. Asia and SG/MY markets trade normally; light global volume expected.

Bottom Line

We are closing the first half of 2026 with a clearer picture than we started with. Micron AI memory 2026 has settled the debate: the AI infrastructure supercycle is real, the revenue is real, and the demand is multi-year. SpaceX’s stumble is a reminder that hype cycles always carry embedded risks — reading the prospectus is not optional. Oil at post-war lows is the most underappreciated macro trade of the moment: if it holds, it simultaneously helps Singapore airlines, hurts Malaysian energy names, and could take the hawkish edge off the Fed. The Great Rotation into value and dividends plays directly to SG/MY investors’ strengths — our markets are cheap, our banks are profitable, and our REITs are finally attractive again relative to US tech. And the AI margin squeeze confirms the picks-and-shovels principle: own the infrastructure, not the application. Practical playbook for the week ahead: watch the Russell reconstitution flows on June 30, monitor Iran deal news for the oil trade confirmation, and keep Keppel DC REIT and Mapletree Industrial Trust on your radar as AI infrastructure compounders. Stay curious, do your own research, and invest for the long term.

For educational purposes only. Not financial advice. Always do your own research. Catch up on last week’s issue: GoodWhale Weekly: Fed Rate Hike 2026 Signal, Oil Crashes Below $80, Intel-Apple US Chip Deal.

Source: CNBC Micron Q3 2026 earnings

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply