The Week in 30 Seconds

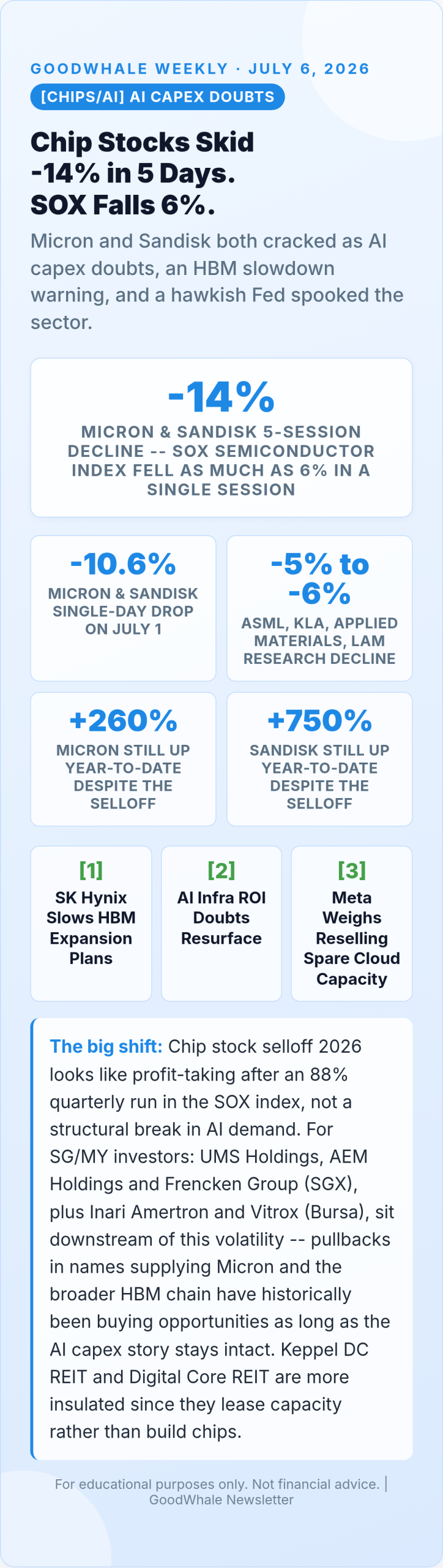

- [CHIPS/AI] Chip stock selloff 2026. Micron and Sandisk each fell 14% over five sessions, SOX index down 6% in a single session, on HBM slowdown reports and AI capex doubts. Both names still up huge YTD.

- [MACRO] Jobs shock, Fed pivot. June payrolls added just 57,000 vs 115,000 expected. Two months of downward revisions. July hike odds fell to 20% from 30%.

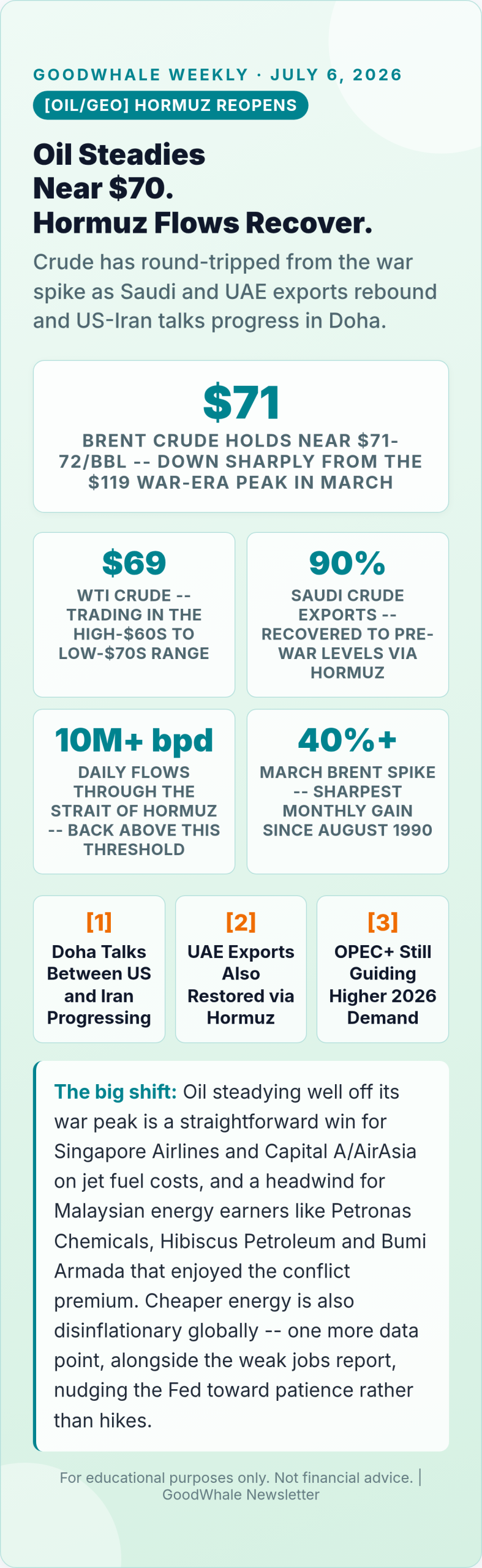

- [OIL/GEO] Oil steadies near $70. Brent at $71-72, WTI near $69, as Saudi and UAE exports recover to ~90% of pre-war levels through the Strait of Hormuz. US-Iran talks progressing in Doha.

- [EARNINGS] Nike’s tariff-boosted beat. Headline EPS $0.72 vs $0.13 estimate, but adjusted EPS just $0.20 after a 52-cent tariff refund. Greater China revenue down 12%.

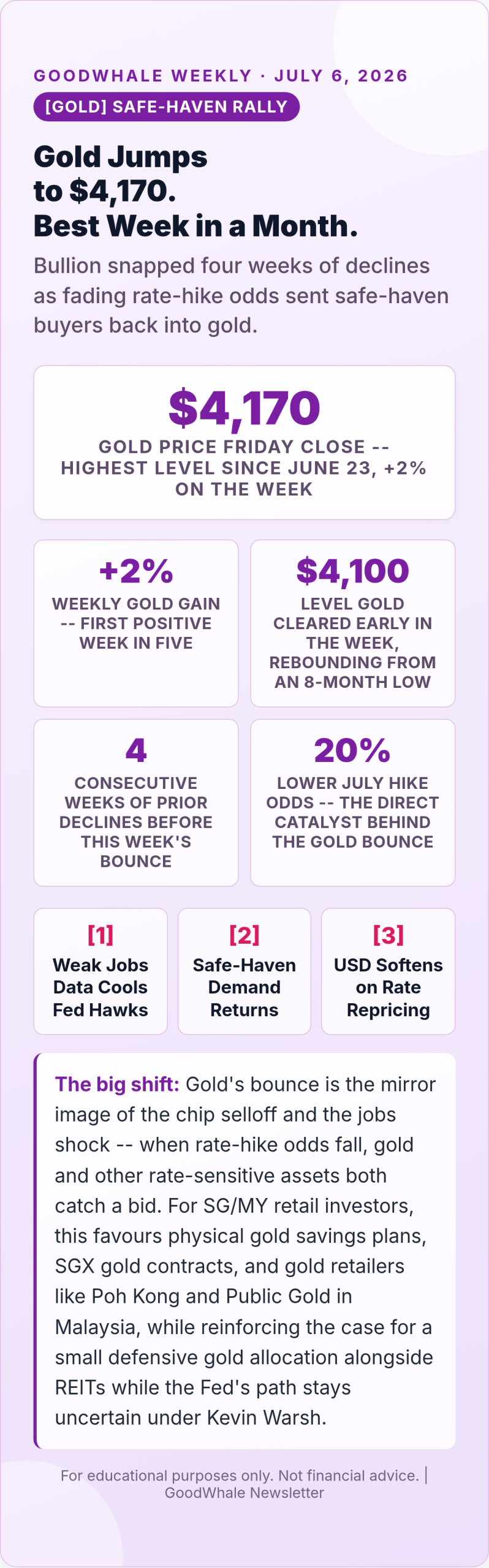

- [GOLD] Gold jumps to $4,170. +2% on the week, snapping four weeks of declines, as fading rate-hike odds revived safe-haven demand.

1. Chip stock selloff 2026: Chip Stock Selloff 2026: Micron, Sandisk Slide as AI Capex Doubts Resurface

Meanwhile, semiconductor stocks had their roughest start to a quarter in months. On Wednesday July 1, Micron and Sandisk each dropped 10.6% in a single session, extending a slide that left both stocks down 14% over five trading sessions. The Philadelphia Semiconductor Index (SOX) — which had rallied an extraordinary 88% in the second quarter — fell as much as 6% in one session on Thursday, its worst two-day skid of the new quarter. Equipment makers were caught in the same downdraft: ASML, KLA Corporation, Applied Materials and Lam Research all lost between 5% and 6%. Even after the rout, both memory names remain deeply in the green for the year — Micron is still up more than 260% and Sandisk more than 750% year-to-date — underscoring just how extended the run had become before this pullback.

The chip stock selloff 2026 traces to a cluster of catalysts landing at once. Reports surfaced that SK Hynix is slowing the pace of its high-bandwidth memory (HBM) capacity expansion, reviving questions about whether AI infrastructure spending will keep generating a commensurate return. Adding to the unease, a report that Meta is exploring a cloud computing business to resell excess data-centre capacity was read by some investors as an early signal of AI infrastructure oversupply. Layered on top: new Fed Chair Kevin Warsh’s increasingly hawkish tone has kept a lid on risk appetite broadly. For SG/MY portfolios, the read-through is nuanced rather than alarming — UMS Holdings, AEM Holdings, Frencken Group, Inari Amertron and Vitrox are the regional picks-and-shovels names most exposed to any near-term wobble in Micron’s supply chain, but none of the news flow this week points to a demand collapse, just a valuation reset after a historic quarter.

| Name | 5-Session Move | 2026 YTD | Sector |

|---|---|---|---|

| Micron (MU) | -14% | +260% | Memory |

| Sandisk (SNDK) | -14% | +750% | Memory |

| Applied Materials (AMAT) | -5% to -6% | n/a | Equipment |

| SOX Index | -6% (1 session) | +88% (Q2) | Index |

2. June Jobs Shock: Payrolls Miss by Half, Fed Rate-Hike Odds Cool

Notably, the Bureau of Labor Statistics dropped a cold bucket of water on the hawkish narrative Wednesday July 2: US nonfarm payrolls rose by just 57,000 in June, less than half the 115,000 economists had expected. The unemployment rate ticked down slightly to 4.2%, but the details underneath were softer than the headline suggests — April’s count was revised down 31,000 to 148,000, and May was cut 43,000 to 129,000, leaving the two-month combined total 74,000 jobs lower than originally reported. Professional and business services led what gains there were, adding 36,000 positions, while leisure and hospitality shed 61,000 jobs — a far weaker read than the usual summer seasonal hiring pattern.

Meanwhile, the market reaction was immediate and squarely about the Federal Reserve. Bloomberg’s rate-probability tracker showed the odds of a hike at the July FOMC meeting sliding to 20%, down from 30% just a week earlier, as traders concluded that new Fed Chair Kevin Warsh — installed in May on the closest confirmation vote in modern Fed history — has less room to lean hawkish than his rhetoric had implied. For SG/MY investors, a softer US labour market and cooling hike odds is a friendly backdrop: it takes pressure off USD strength, which in turn eases the tightening burden on MAS’s S$NEER policy band and supports both the Singapore dollar and ringgit. Rate-sensitive REITs and dividend payers stand to benefit most if this data trend persists into the back half of the year.

3. Oil Steadies Near $70 as Strait of Hormuz Shipping Recovers

However, crude prices have quietly normalised after one of the wildest stretches in years. Brent held near $71-72 per barrel and WTI traded around $69 this week, both a long way down from the $119 peak Brent touched in March when the US-Israel-Iran conflict first closed the Strait of Hormuz and triggered the sharpest monthly oil spike since August 1990. The turnaround has been driven by a genuine recovery in shipping: Saudi Arabia’s crude exports have rebounded to roughly 90% of pre-war levels, the UAE has also restored its exports to pre-war volumes by routing tankers back through Hormuz, and total daily flows through the strait are now running above 10 million barrels once again.

The diplomatic backdrop is helping. US President Trump said talks with Iran were progressing well after mediators from Qatar and Pakistan wrapped separate meetings with US and Iranian negotiators in Doha this week. OPEC, for its part, continues to guide toward robust 2026 demand growth of roughly 1.4 million barrels per day, with the UAE — no longer bound by OPEC quotas — pushing harder to win long-term Asian market share. For SG/MY investors the rotation is clean: lower, steadier oil is a direct tailwind for Singapore Airlines and Capital A/AirAsia through cheaper jet fuel, while it squeezes the earnings power of Malaysian energy names such as Petronas Chemicals, Hibiscus Petroleum and Bumi Armada that had benefited from the war-era premium. It is also one more disinflationary data point that, alongside this week’s soft jobs report, argues for a more patient Fed.

4. Nike Q4 FY2026: Tariff Refund Masks a Soft China Quarter

Additionally, nike’s fiscal Q4 2026 results, reported Tuesday June 30, were a lesson in reading past the headline. Revenue came in at $10.97 billion versus $10.86 billion expected, and EPS of $0.72 blew past the $0.13 estimate — but the beat was almost entirely a one-off. Roughly 52 cents of that EPS came from an expected IEEPA tariff refund, leaving adjusted EPS at just $0.20. Regionally, North America grew a modest 3% to $4.83 billion and EMEA slipped 1% to $2.98 billion, but the standout weak spot was Greater China, down 12%. By channel, Nike Direct revenue fell 7% on a reported basis (9% currency-neutral) while wholesale revenue rose 4%, suggesting Nike’s own stores and app are struggling more than its retail partners.

Full-year fiscal 2026 net income landed at $3.11 billion ($2.10 per share), down from $3.22 billion ($2.16 per share) a year earlier — a reminder that even a headline-beating quarter can mask a business still working through a turnaround. For SG/MY investors, the China weakness is the more important signal than the tariff-flattered EPS: it echoes a broader pattern of cautious Chinese consumer spending that shows up across regional retail, travel and e-commerce names with China exposure, from mall REITs to logistics operators serving cross-border trade. The takeaway is not to avoid Nike, but to always strip out one-time items — tariff refunds, buybacks, asset sales — before deciding whether an earnings beat reflects real operating momentum.

5. Gold Jumps to $4,170 as Rate-Hike Odds Fade

On the other hand, gold quietly had one of its better weeks of the year. Bullion pushed above $4,100 an ounce early in the week, rebounding from an eight-month low, then climbed further to close Friday at $4,170 — its highest level since June 23 and a 2% weekly gain that snapped four straight weeks of declines. The catalyst was straightforward: as markets absorbed Wednesday’s weak US jobs report and pushed the odds of a July Fed hike down to 20% from 30%, the dollar softened and safe-haven demand for gold picked back up. It’s worth noting the scale of the year’s moves in context — gold touched an all-time high above $5,595 back in late January before retreating, so this week’s bounce is a recovery within a much larger, more volatile 2026 range rather than a fresh record.

For SG/MY retail investors, gold’s renewed strength is a timely reminder of its role as a portfolio stabiliser precisely when other risk assets — like this week’s chip stocks — are wobbling. Local gold savings plans, SGX gold futures, and physical retailers such as Poh Kong and Public Gold in Malaysia all benefit directly from firmer bullion prices, and a modest gold allocation continues to make sense as a hedge while Fed Chair Kevin Warsh’s actual policy path remains genuinely uncertain. The through-line across this week’s five stories is consistent: soft US data is repricing Fed expectations lower, and that repricing is rippling through chips, oil, jobs-sensitive equities and now gold all at once.

What I’m Watching Next Week

Key data and events — July 6 to July 10

- Mon 6 Jul — Quiet start post-Independence Day; light US earnings and data calendar; watch Asia open for follow-through on the chip selloff.

- Tue 7 Jul — NFIB Small Business Optimism (June); Singapore and Malaysia market reaction to the softer US jobs print continues to play out.

- Wed 8 Jul — FOMC minutes from the June meeting — markets will parse every line for how much weight Chair Warsh puts on labour-market weakness.

- Thu 9 Jul — US initial jobless claims (a live read on whether the June payrolls miss was a one-off or a trend); continued watch on Doha talks for oil.

- Fri 10 Jul — Big US bank earnings season begins to come into view over the following week; a natural checkpoint for how Q2 2026 shaped up broadly.

Bottom Line

Five very different headlines this week — chips, jobs, oil, sneakers, gold — all trace back to the same thread: incoming data is repricing how hawkish the Fed under Kevin Warsh can actually be, and every asset class is adjusting in real time. The chip stock selloff 2026 is a valuation reset after an extraordinary run, not evidence the AI capex cycle is broken. A weak jobs report and cooling hike odds is a tailwind for SG/MY REITs, banks and currency stability. Oil steadying near $70 helps Singapore’s airlines and hurts Malaysia’s energy earners. Nike’s China weakness is a signal worth watching for any business with Chinese consumer exposure. And gold’s bounce is a reminder that a small defensive allocation earns its keep exactly during weeks like this one. Practical playbook: watch Wednesday’s FOMC minutes for how much weight Warsh puts on the labour data, keep an eye on further Hormuz shipping data, and treat any further chip-sector weakness as a valuation question, not a demand question, before deciding whether to add to positions.

For educational purposes only. Not financial advice. Always do your own research. Catch up on last week’s issue: GoodWhale Weekly: Micron AI Memory 2026 Blowout, SpaceX Bond Shock, Oil at Post-War Lows.

Source: Bloomberg chip stocks report

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply