The Week in 30 Seconds

- ☁️ Cloud Trio crushed Q1. Alphabet +10% in a day. Azure +39%, AWS +28%. Enterprise AI hits the revenue line.

- 💸 Meta beat — got punished. Capex hiked to $145B. Stock −7%. Big Tech AI capex now >$650B in 2026.

- 🍎 Apple picks Google. Q2 rev $111.2B (+17%). New Siri runs on Gemini. Distribution > development.

- 🏛️ Fed held, four dissented. Most dissent since 1992. Powell’s final meeting. Dovish successor priced in.

- 🛢️ Brent $126 → $108. Iran peace proposal cooled the war premium. Hormuz still 20% disrupted.

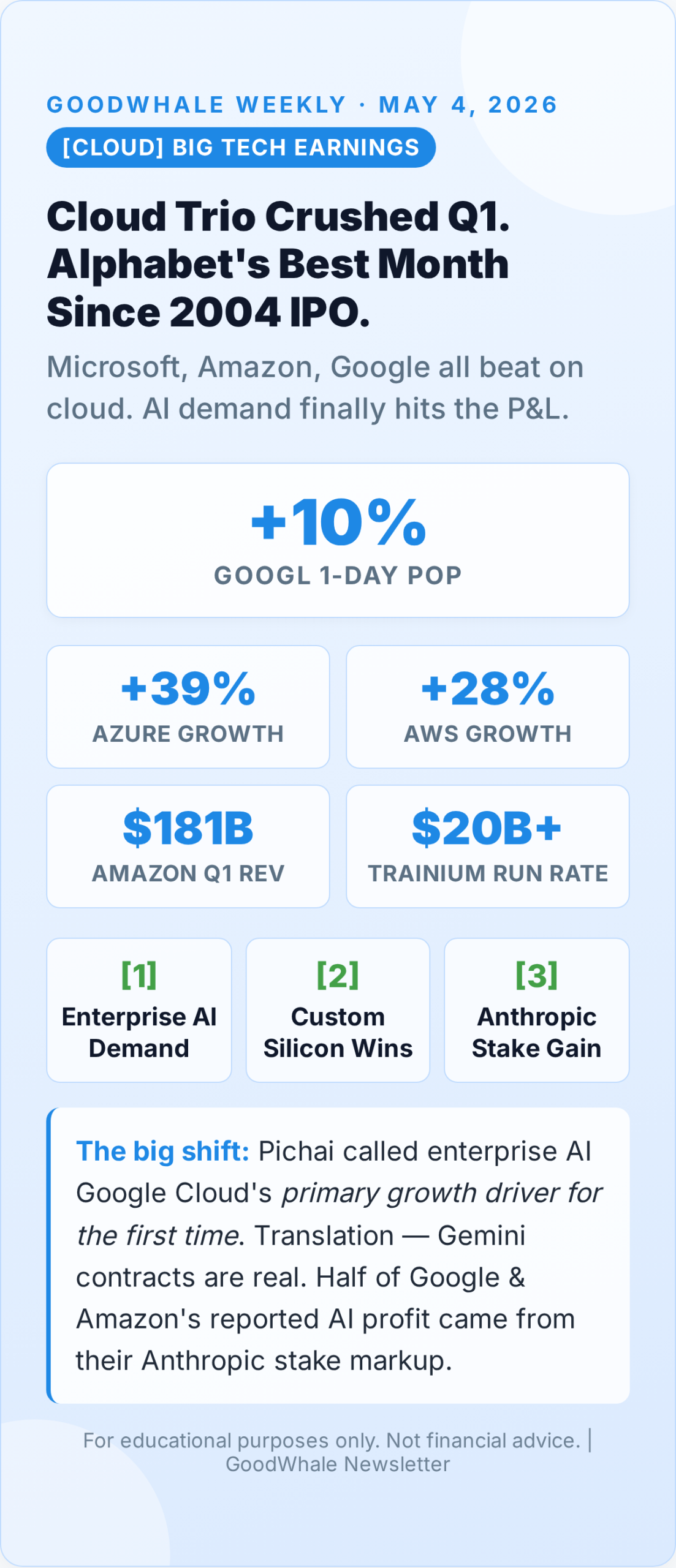

1. Big Tech’s Cloud Trio All Beat Q1 — Alphabet’s Best Month Since 2004

All three hyperscalers crushed Q1 on the same calendar. Alphabet popped 10% in a day, its best month since the 2004 IPO. Azure ran +39%, AWS hit +28%. Sundar Pichai’s quote stuck out: “Enterprise AI is now Google Cloud’s primary growth driver for the first time.” Three years of AI capex finally showing up on the revenue line, not just the cost line.

If you hold US tech ETFs (CSPX, VWRA, NDQ) you’re already long this trade. Local proxy: Singtel’s Nxera Bukit Timah data centre serves exactly this enterprise AI workload.

| Hyperscaler | YoY Growth | Q1 Cloud Rev | 1-Day Move |

|---|---|---|---|

| Microsoft Azure | +39% | $32.1B | +5.4% |

| Amazon AWS | +28% | $30.8B | +3.1% |

| Google Cloud | +34% | $13.4B | +10.0% |

2. Meta’s Capex Hits $145B Top-End — Stock Drops 7% Despite the Beat

Meta beat. Then Meta got punished. Q1 revenue $56.3B (+33%), net income +61%, EPS $7.31 vs $6.79 expected — a print that should have triggered a 5% rip higher. Instead the stock dropped 7% after-hours. Capex guidance was raised to a top end of $145 billion, the second hike this year. Add it up across the four hyperscalers: Big Tech is on track to spend over $650B on AI infrastructure in 2026 — a number Wall Street has never had to model.

Singapore data centre operators (Keppel DC REIT, Digital Core) sit upstream of this capex wave. They benefit even if Meta’s stock chops sideways.

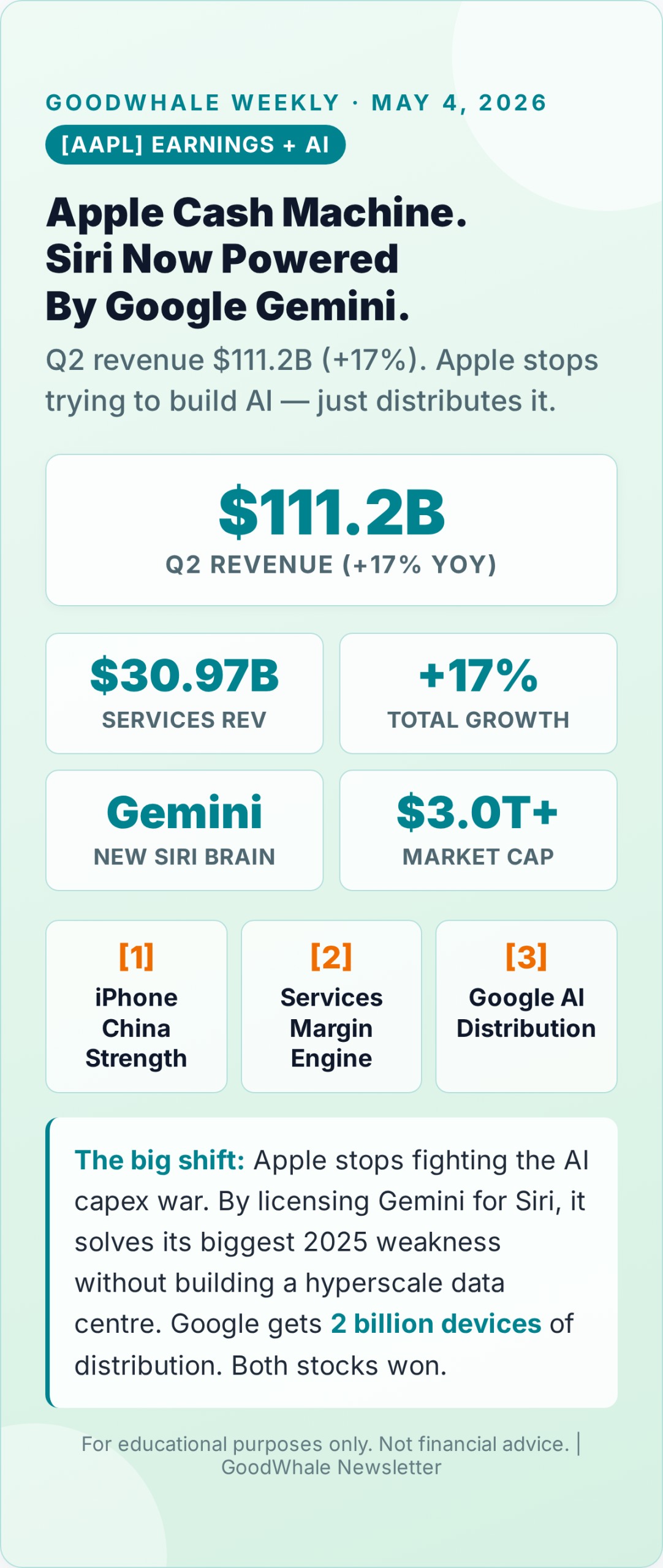

3. Apple Picks Google Gemini to Power New Siri

Apple’s quarter was clean: $111.2B revenue (+17%), services at a record $30.97B, market cap above $3T. The news was buried in the call — Apple signed a multi-year deal to power the new Siri on Google Gemini. After two years of failing to ship competitive on-device AI, Tim Cook chose distribution over development. Apple sidesteps the $50–100B annual capex bill its peers are locked into; Google gets two billion devices of Gemini distribution. Both stocks finished green.

The question stops being “who builds the best model” and becomes “who owns the consumer endpoint.” This week the answer was Apple.

4. Fed Holds at 3.75% With Four Dissents — Most Since 1992

On the surface the Fed did nothing — held at 3.75%, kept the dot plot at one cut for 2026. The story was under the surface: four dissents, the most at a single FOMC meeting since 1992. Miran wanted a 25bp cut now; Hammack, Kashkari and Logan rejected any easing bias on sticky services inflation. This was Powell’s last meeting as chair — he hands the gavel on 15 May, and markets are pricing a more dovish successor: DXY at multi-year lows, USD/SGD at 1.27.

Weaker USD plus a more dovish Fed is textbook fuel for SG REITs (CICT, MLT, Mapletree PanAsia) and high-dividend banks (DBS, OCBC, Maybank). Hold quality through the chair transition.

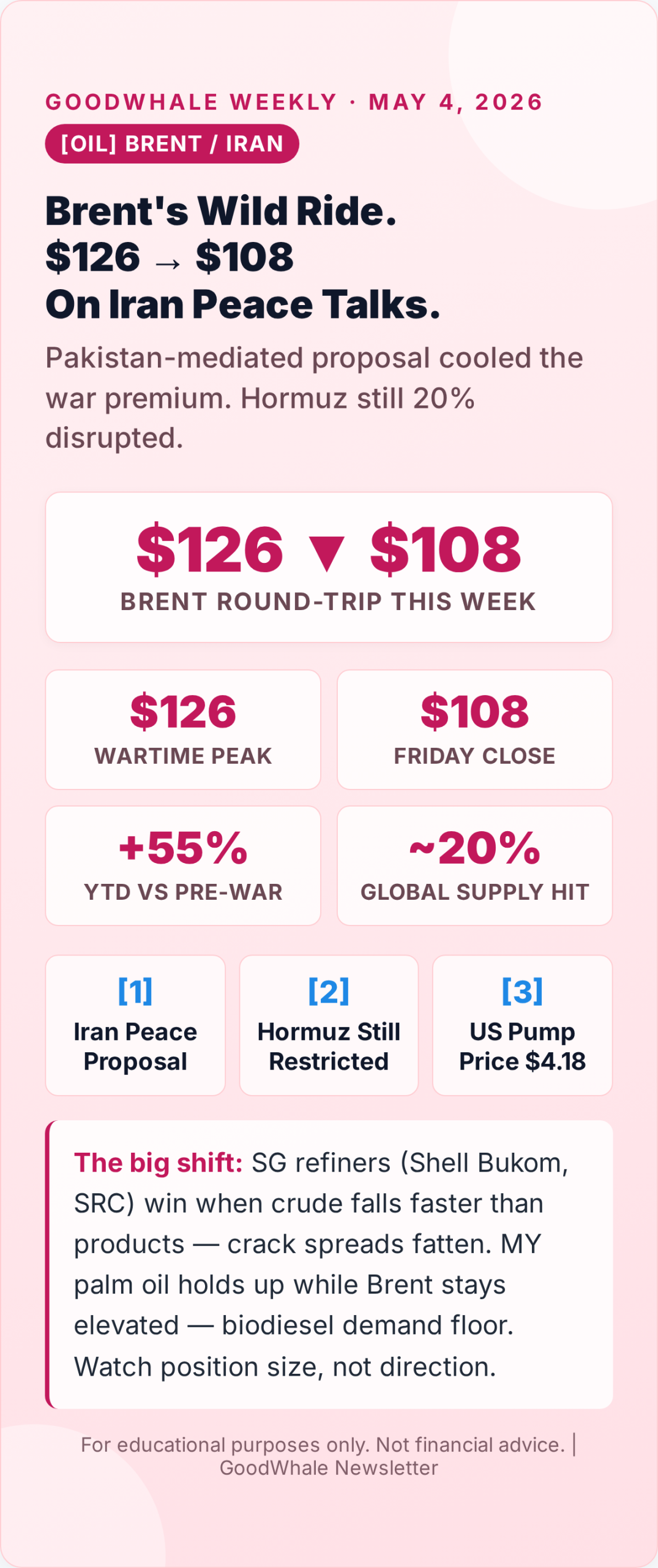

5. Brent Crashes from $126 to $108 on Iran Peace Proposal

Brent went on a tour. Opened around $122, spiked to $126 mid-week on a fresh Hormuz incident, then crashed to $108 by Friday after Pakistan-mediated talks produced an Iran peace proposal — which hasn’t been signed. The war premium is thinner now, but the structural premium isn’t gone: Hormuz is still ~20% below normal, crude is still up roughly 55% from pre-war levels. Base case for 2026: $95–115 with periodic spikes.

Singapore refiners (Shell Bukom, SRC) benefit when crude falls faster than products — crack spreads fatten. MY palm oil holds a structural floor as long as Brent stays above $90. Size for volatility, not direction.

What I’m Watching Next Week

Calendar items that could move portfolios

- 15 May — Powell’s last day as Fed Chair. Markets will price the new chair’s first read.

- SG GDP advance estimate — Q1 print due. A beat lifts STI banks (DBS, OCBC, UOB).

- Walmart, Cisco, Alibaba earnings — consumer + China AI infrastructure read-through.

- OPEC+ ministerial — first meeting since the Iran proposal. Moves Brent and SG refiners.

- Bursa plantations (KLK, IOI, SDP) — CPO floor watch if Brent settles above $90.

Bottom Line

AI capex is real but the bill is now visible. The Fed has lost consensus. Oil reminded everyone geopolitics is a feature, not a bug. For a SG/MY retail investor, the question isn’t which name to chase — it’s: does my portfolio still make sense in a world of $650B Big Tech capex, a 4-way Fed split, and Brent in a $90–115 range? If yes, hold. If no, the next month is your window.

For educational purposes only. Not financial advice. Always do your own research.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

[…] Previous […]