The Week in 30 Seconds

- 🏛️ Warsh confirmed Fed chair. 54-45 vote — closest in modern Fed history. June 17 FOMC is the real test.

- 🔥 April CPI 3.8%. Hottest since May 2023. Energy +17.9%. Friday saw all three US indices fall >1%.

- 💥 Cisco +15%. Best single-day pop since 2002. AI orders $5.3B YTD; FY guide raised to $9B; 4,000 jobs cut.

- ☁️ Alibaba split. Cloud +38%, AI run-rate $5.3B (30% of external cloud). But net profit -99.7% on AI capex.

- 🛢️ Brent back to $109. Hormuz still 95% empty. IEA flags undersupply risk through October.

1. Warsh Fed chair: Warsh Wins It — Confirmed Fed Chair 54-45, Closest Vote of the Modern Era

Meanwhile, kevin Warsh was confirmed Fed chair Wednesday May 13 by a 54-45 Senate vote — the narrowest margin since chair confirmation votes have been recorded. Only one Democrat, John Fetterman, crossed the aisle. Powell drops to a regular governor seat (term runs to early 2028); Warsh runs his first FOMC on June 16-17, complete with fresh dot plots.

The political subplot is the whole story. President Trump has made it very public he wants rate cuts, and Democrats spent the hearings warning Warsh would be a “sock puppet.” Warsh’s own pitch: cut the policy rate, tighten the balance sheet, and use his own judgment. Markets are pricing one to two cuts by year-end. For SG/MY portfolios, a perceived political pivot weakens USD — bullish REITs and EM equities. But if the long end revolts (10Y > 4.7%), it’s a credibility crisis, not a pivot. Watch DBS, OCBC, UOB carefully too: lower short rates squeeze NIM, but credit volumes lift.

| Confirmation Vote | Chair | Year | Vote |

|---|---|---|---|

| Kevin Warsh | Chair (Trump) | 2026 | 54-45 |

| Jerome Powell (2nd term) | Chair (Biden) | 2022 | 80-19 |

| Jerome Powell (1st term) | Chair (Trump) | 2018 | 84-13 |

| Janet Yellen | Chair (Obama) | 2014 | 56-26 |

2. April CPI Hit 3.8% — Hottest Since May 2023, Friday Wiped Out the Highs

Notably, tuesday May 12 dropped a hot one. Headline CPI ran +0.6% m/m and +3.8% y/y, the highest annual print since May 2023, up from March’s 3.3%. Core CPI ticked +0.4% m/m, 2.8% y/y. The biggest single contributor: energy +17.9% y/y, the steepest annual gain since September 2022 — the direct fingerprint of an oil market still pricing 4 mbpd of Hormuz disruption.

Markets shrugged on Wednesday, then on Friday May 15 the S&P, Nasdaq and Dow all fell more than 1% as the 10Y yield jumped. CME futures briefly priced a ~30% probability of a rate hike by year-end. For SG/MY readers: hot US CPI = stronger USD. USD/SGD ticked up to 1.324, and MAS has already tightened its S$NEER slope in April for exactly this reason. Keep your USD T-bill / MMF ladder alive at 4%+. SGX, ICE-listed exporters and Bursa palm-oil names benefit on USD revenue translation.

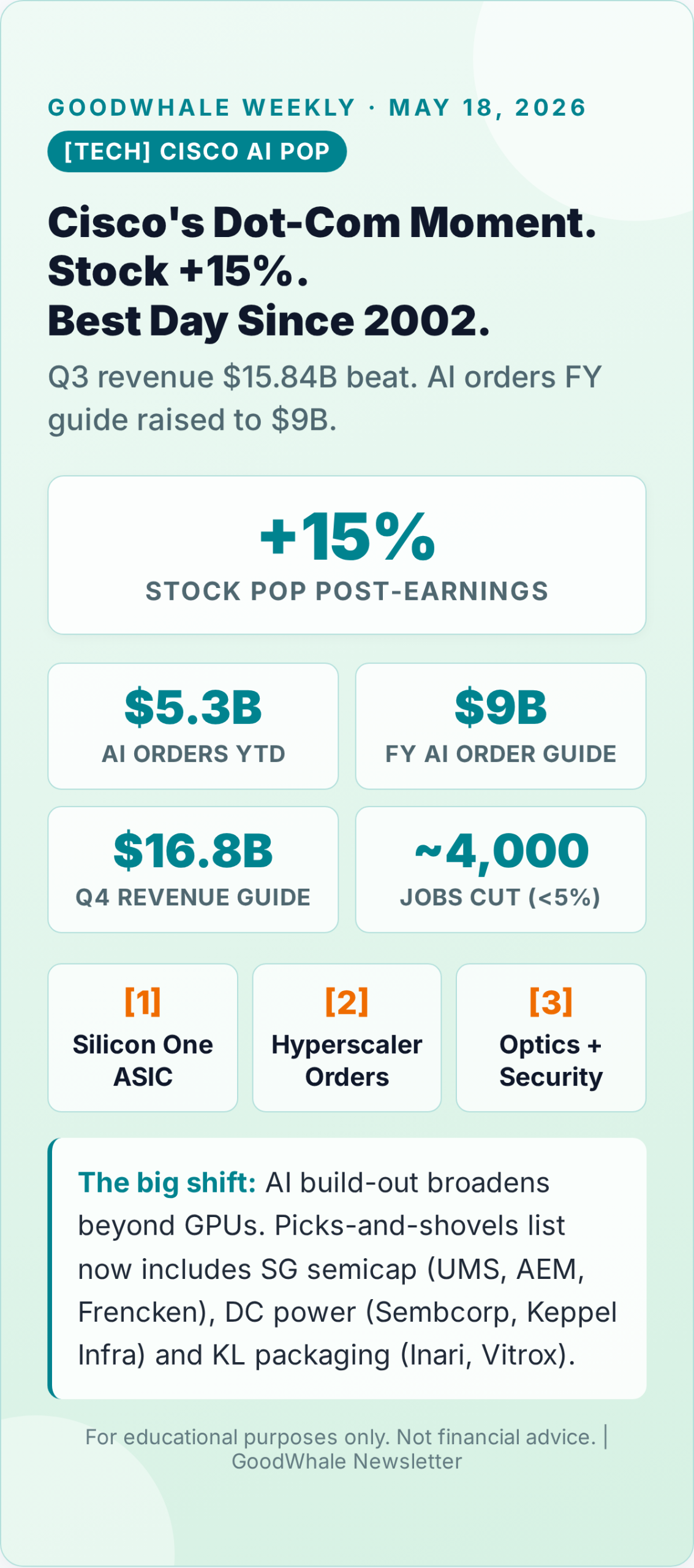

3. Cisco’s Dot-Com Moment — +15% Pop, $9B AI Order Book, 4,000 Jobs Cut

However, wednesday May 13 after-bell: Cisco posted Q3 FY26 revenue of $15.84B (beat $15.56B), EPS of $1.06, and dropped two bombs — AI infrastructure orders YTD have hit $5.3B, and full-year guidance jumped to $9B, up from $5B prior. Networking is no longer the boring part of the AI build-out.

The stock popped +15% in extended trading, the sharpest single-day rally since 2002 — that’s the post-dot-com-crash bounce. About $70B of market cap got added overnight. The pivot: Cisco is cutting fewer than 4,000 jobs (under 5%) while shifting headcount into silicon (Silicon One ASICs), optics, security, and AI-infrastructure systems. CEO Chuck Robbins framed it as “intentional redirection,” not a cost-cut. The SG/MY angle: the picks-and-shovels list just got longer. SG semicap (UMS, AEM, Frencken), DC power (Sembcorp, Keppel Infra), KL packaging (Inari Amertron, Vitrox) all sit upstream of this networking-and-optics build-out.

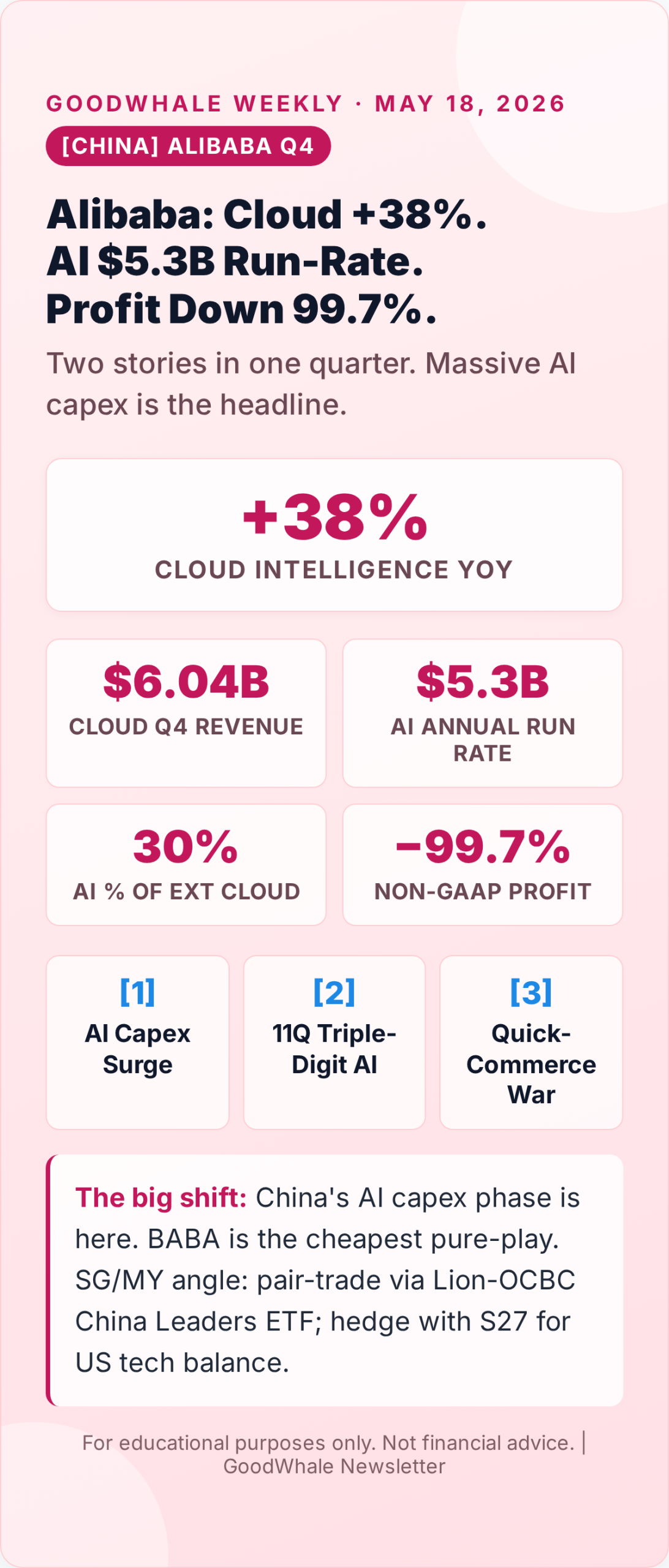

4. Alibaba Q4: Cloud +38% and AI Run-Rate $5.3B — But Profit Cratered 99.7%

Additionally, same night, May 13, Alibaba’s Q4 FY26 told two different stories. Revenue: $35.28B (+3% YoY) — a touch light. But Cloud Intelligence Group revenue ran RMB 41.6B ($6.04B), +38% YoY, with external cloud growth accelerating to +40%. AI product revenue posted triple-digit growth for the 11th consecutive quarter and hit a $5.3B annual run rate — AI is now 30% of external cloud revenue.

The catch: non-GAAP net profit collapsed -99.7% to RMB 86M as the company plowed everything into AI capex, cloud infrastructure, and quick-commerce competition with JD/Meituan. Management says margins will be ugly for several quarters — they want to capture share while it’s available. This is the “AI investment phase” the US hyperscalers ran through in 2024-25, but happening in Hangzhou. For SG/MY retail, BABA (or HKEX-listed 9988) is the cheapest pure-play on Chinese AI capex. Pair-trade idea: long BABA cloud growth via Lion-OCBC China Leaders ETF, hedged against US tech via S27/IVV.

5. Brent Back to $109 — Hormuz Still at 5% of Normal Vessel Flow

On the other hand, last week Brent crashed to $101 on ceasefire optimism. This week it rebuilt to $109.26 (+7.9% wk) as the April 8 US-Iran ceasefire kept getting violated. Iran’s foreign minister told reporters May 15 that “lack of trust” is blocking negotiations. The IEA flagged that crude/fuel flows through the Strait fell ~4 mbpd in March-April, and even if the conflict ends “next month,” the global market could stay materially undersupplied through October.

The hard data: pre-conflict, around 3,000 vessels transited Hormuz each month. Right now — ~5% of that. Markets are in a strange equilibrium: oil grinds higher on no news, dumps on ceasefire headlines, rips on Iranian provocation. April CPI energy +17.9% told you the macro cost. Q2 corporate margins will tell you the corporate cost. SG winners on sustained $100+ Brent: Seatrium, Beng Kuang Marine, Marco Polo Marine. KL winners: Petronas Chemicals, Hibiscus Petroleum, Bumi Armada. Losers: SIA, AirAsia (Capital A), Genting on jet fuel + travel demand. Don’t chase headlines; size for both the ceasefire dump and the next escalation pop.

What I’m Watching Next Week

Calendar items that could move portfolios

- Tue 19 May — Home Depot, Palo Alto Networks earnings; Singapore NODX April (export pulse).

- Wed 20 May — FOMC minutes (April meeting); Target, TJX earnings (US consumer health).

- Thu 21 May — Nvidia Q1 FY27 — the AI capex bellwether; Walmart Q1; Singapore CPI April.

- Fri 22 May — US PMI flash (May); UMich consumer sentiment; ECB minutes.

- All week — Warsh’s first speeches as chair; Iran/Hormuz headlines; the oil tape.

Bottom Line

A new Fed chair walks in with a hot CPI tape, oil structurally bid, and the AI build-out broadening from GPUs to networking, optics and Chinese cloud. For a SG/MY retail investor, the question isn’t which name to chase — it’s: does my portfolio survive a year where the Fed cuts under political pressure, USD chops on credibility, and Brent sits in a $95-115 range? Quality compounders, USD T-bill ladder at 4%+, and a tight watchlist of REITs and SG/MY semicap names is how I’d play it. The next four weeks — Nvidia earnings, Warsh’s first FOMC — are the test.

For educational purposes only. Not financial advice. Always do your own research. Catch up on last week’s issue: GoodWhale Weekly: Cloud Trio Beats, Meta’s $145B Capex, Brent’s Wild Ride.

Source: CNBC

{kind=link}

{kind=link}

{kind=link}

{kind=link}

[…] Previous […]