The Ministry of Health (MOH) has announced major IP rider changes in Singapore that will reshape how hospital insurance works from 1 April 2026.

If you already have a private hospital insurance plan, are planning to buy one, or are simply confused by the headlines, this article will help you understand what is really changing and why.

Instead of fear or urgency, the goal here is clarity. Once you understand how hospital bills are actually paid in Singapore, the MOH IP rider changes will make much more sense.

Watch the Full Explanation Video

Below is the full YouTube video where I walk through the MOH IP rider changes step by step, including real bill examples and how this affects different groups of people.

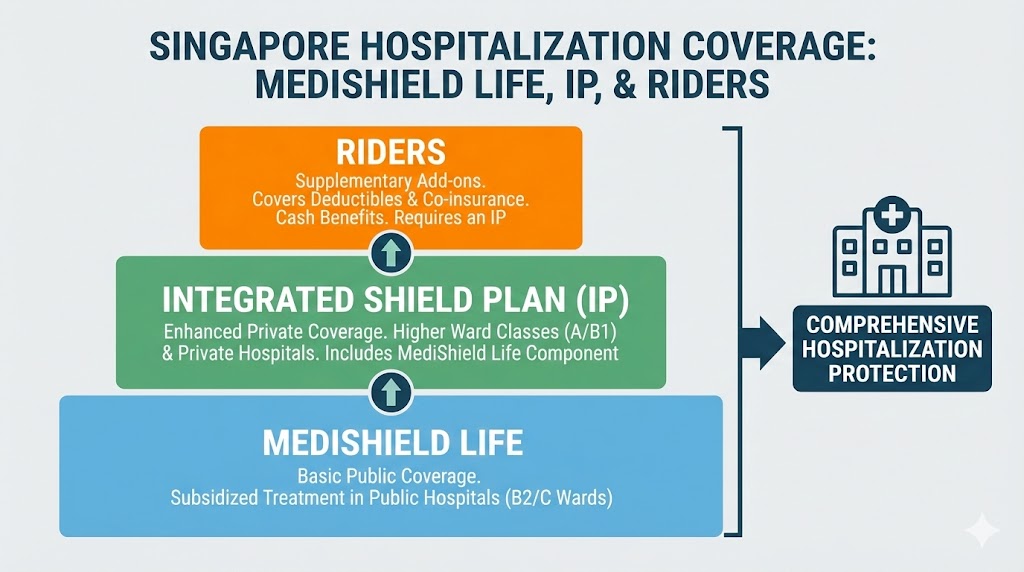

How Hospital Insurance Works in Singapore

To understand the MOH IP rider changes, you first need to understand the structure of hospital insurance in Singapore.

There are three main layers. Medishield Life, Integrated Shield Plans and Riders.

If you are not sure how much are you paying for your health insurance, do check out CPF’s Health Insurance Planner. It will be helpful to know how your expenses to health insurance will change over time too!

Anyways, I have broken down in layman for you to understand.

MediShield Life

MediShield Life is the basic national health insurance that covers all Singaporeans and permanent residents. It helps to cover large hospital bills, mainly in subsidised wards.

Integrated Shield Plans (IPs)

Integrated Shield Plans sit on top of MediShield Life. They provide higher coverage for public hospital A-class wards or private hospitals, depending on the plan you choose.

Riders

A rider is an optional add-on to your Integrated Shield Plan. Riders are designed to reduce how much cash you need to pay out of pocket, especially deductibles and co-payments. Riders are always paid using cash, not Medisave.

This layered structure is important, because hospital insurance in Singapore is not designed to make hospitalisation free. It is designed to prevent a medical bill from becoming a life-changing financial problem.

How Hospital Bills Are Actually Paid (Step-by-Step)

One of the biggest misunderstandings about hospital insurance is how payment actually works when a real hospital bill arrives.

Let’s use a realistic private hospital bill of $80,000 as an example.

Step 1: Deductible

The deductible is the amount you must pay first every policy year before insurance starts paying. For many private hospital plans, this can be around $3,500.

Step 2: Insurance Pays the Bulk

After the deductible, your Integrated Shield Plan typically pays around 90 percent of the remaining bill.

Step 3: Co-payment

Without any rider, most private Integrated Shield Plans require a 10 percent co-payment. For an $80,000 bill, this can mean more than $7,000 in cash.

In total, even with insurance, your out-of-pocket cost can easily exceed $11,000. This is why riders were introduced in the first place.

Why IP Riders Exist

IP riders were designed to reduce cash shock during serious hospitalisation. Even with insurance coverage, coming up with deductibles and co-payments during a medical emergency can be stressful.

However, there is a trade-off. Riders are paid every year, even though most people are not hospitalised often. Over time, this led to higher claims, rising premiums, and a system that became harder to sustain.

This tension is at the heart of the MOH IP rider changes in Singapore.

The Mismatch Problem in Singapore Healthcare

Data has shown that many Singaporeans who buy private hospital insurance still choose subsidised public wards when hospitalised.

This mismatch means people are paying higher premiums for coverage they may not fully use, while public healthcare continues to shoulder much of the demand. Combined with rising medical inflation, this contributes to premium increases that affect the middle class the most.

What MOH Changed in November 2025

In November 2025, MOH announced new requirements for IP riders that will take effect from 1 April 2026.

Under the new rules:

- IP riders can no longer fully cover the minimum deductible

- Co-payment caps are increased to ensure patients remain aware of costs

The intention of these MOH IP rider changes is not to remove protection, but to restore cost awareness and long-term sustainability.

Recent News: IP Riders Will Cease Sales

Recent reports highlighted that almost all current IP riders will stop being sold from 1 April 2026.

Insurers can continue selling existing riders until 31 March 2026, but riders purchased from 27 November 2025 will eventually transition to new compliant riders by the next renewal after 1 April 2028.

This is why many people feel confused or pressured, even though there is no need to rush.

What the MOH IP Rider Changes Mean for You

The impact of the MOH IP rider changes depends on which group you belong to.

1. If You Never Bought Hospital Insurance

You are already covered by MediShield Life. This is a preference decision, not a fear decision. The key is understanding what trade-offs you are comfortable with.

2. If You Bought Before 27 November 2025

Your existing rider is not cancelled. Your coverage remains as stated in your policy document. The most important step is reviewing your coverage and understanding what you are paying for.

3. If You Bought After the Announcement or Are Planning to Buy

You will eventually transition to new IP riders. These riders are expected to cost less, and the savings can be redirected towards emergency funds, retirement, or long-term investments.

My Personal View on the MOH IP Rider Changes

I believe the MOH IP rider changes are meant to fix a system that was becoming unsustainable.

Insurance should protect against major financial shocks, not remove all cost awareness. When coverage becomes too generous, premiums rise and hurt those who need protection the most.

The key is education. When people understand how hospital insurance works in Singapore, they can make decisions based on clarity instead of fear.

Final Thoughts

Hospital insurance is not meant to make healthcare free. It is meant to protect you from bills that can derail your life.

The MOH IP rider changes in Singapore are a reminder to understand what you are paying for, what you value, and what you can afford long term.

Clarity matters more than rushing. And peace of mind only works when it is sustainable.

If you need someone to look through your coverage and have better clarity, do reach out to me here.

If this information is useful, do share it with your family and friends.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply