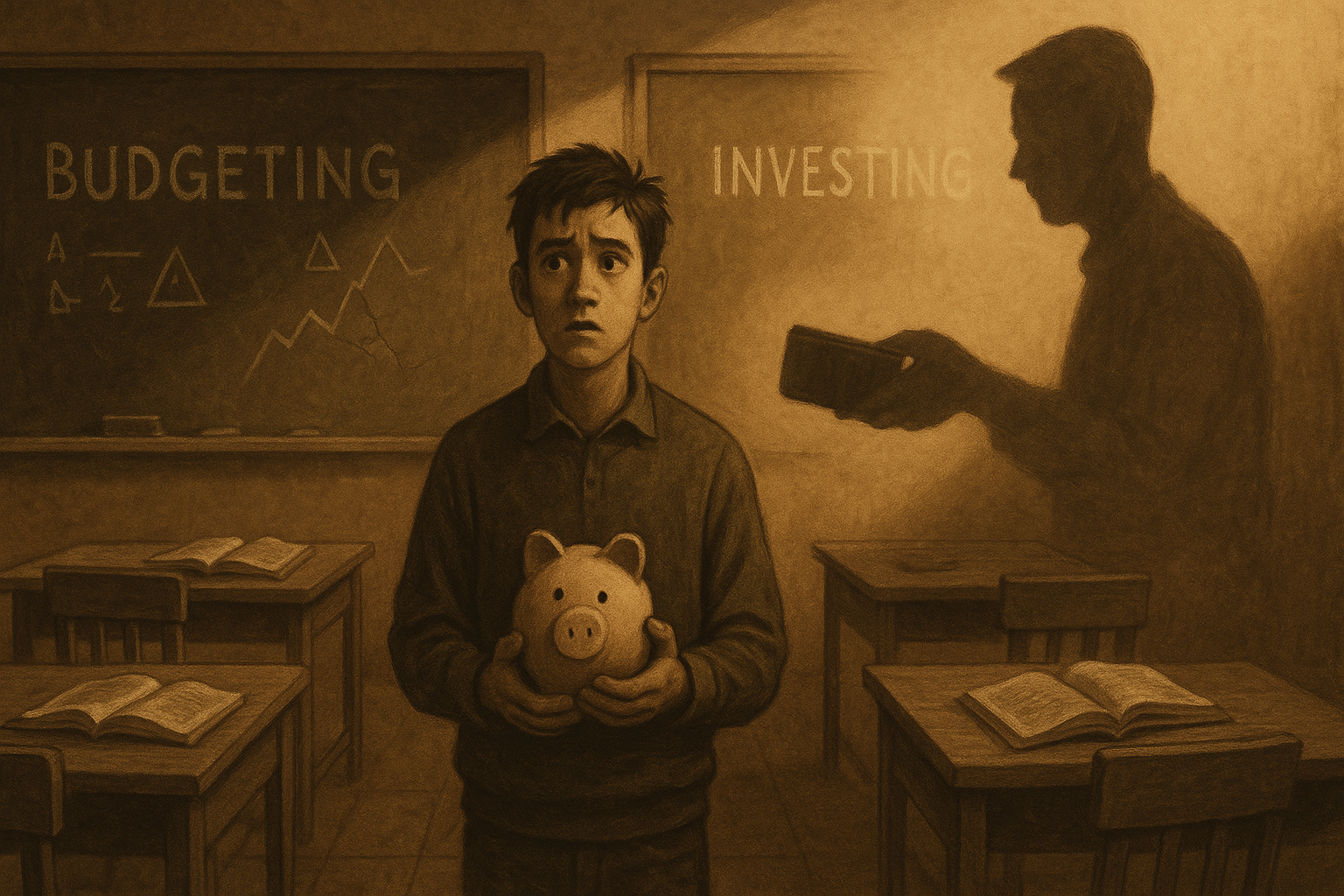

We came across this article by Erin Lowry recently and found it both bold and thought-provoking. The piece challenges Gen Z’s approach to money and argues that they have no excuse for being financially illiterate, given the resources at their fingertips. But as we read it, we couldn’t help but feel that the story runs deeper than just “information access.” So we’d like to share some of our thoughts—our lens—on what’s really happening behind these trends, and why the real conversation should be about belief, not just knowledge.

Information Is Everywhere. So Why Are So Many Still Lost?

After reading Erin Lowry’s piece, I get where she’s coming from. On paper, Gen Z has every advantage: access to investing apps, personal finance TikToks, budget spreadsheets, crypto, robo-advisors, free credit scores—you name it. They’re the most connected generation in history.

But let’s not confuse access with action. Or even understanding.

This reminds me of something from the book 這輩子賺多少才夠 (roughly translated: “How Much Is Enough for This Life?”):

“Information is not knowledge. And knowledge is not action.”

The real question is not do they know enough, but do they care enough to act on it?

It’s Not Ignorance. It’s Distrust.

Erin points out that nearly half of Gen Z thinks saving for the future is pointless. That’s not laziness. That’s disillusionment.

They’ve grown up watching their parents grind away at 9–5s, only to retire stressed and broke. They’ve seen inflation kill purchasing power, witnessed housing become unaffordable, and watched the stock market turn into a roulette wheel driven by headlines, memes, and Elon tweets.

So when a 23-year-old says, “What’s the point of saving?” — they’re not being stupid. They’re telling you:

“I’m not sure I believe the system works.”

That’s the part we need to talk about more.

Schools Can’t Teach What Parents Never Learned

Erin is right that a single high school class won’t magically turn teens into savvy investors. You can’t expect a non-finance teacher to teach compounding interest and asset allocation in 12 weeks and expect it to stick.

The deeper issue is this: Financial behavior starts at home.

As 這輩子賺多少才夠 puts it, money habits are emotional, not just logical. Kids observe more than we think. When they see their parents living paycheck to paycheck, spending impulsively, or stressing about bills—they absorb that.

We’re not just teaching money. We’re transferring beliefs.

Social Media is the Wild West of Finance

Sure, TikTok has a ton of #FinTok creators. But for every one who preaches slow wealth-building, there are ten pushing leverage, crypto pumps, or get-rich-quick scams dressed as “side hustles.”

This generation doesn’t lack content. They lack filtering skills.

And when everyone claims to be an “expert,” the loudest voice wins. Which is why I always say:

“Financial literacy in 2025 means not just knowing what to do—but knowing who to listen to.”

The Real Problem: They Don’t Know Why Money Matters

Erin closes by saying Gen Z has “virtually no excuse” for financial illiteracy. I agree—on a technical level. The resources are out there. But here’s what’s missing:

“Money doesn’t motivate people. Meaning does.”

If you don’t know what kind of life you want to build, no app or budget tool will help. Without clarity, finance feels like another task to avoid—not a tool to be excited about.

That’s what I think a lot of Gen Z needs—not more tips, but more truth. Not just “how to save,” but what they’re saving for.

Summary: The Problem Isn’t Money. It’s Meaning.

Yes, Gen Z has more financial resources than any generation before. But information alone doesn’t lead to transformation. They’re not failing because they’re uninformed. They’re stuck because they don’t see the point.

The real question isn’t, “How do I invest?” It’s, “What kind of life am I building—and what role does money play in that?”

Once that question is clear, the learning follows naturally. Because when you find meaning, you’ll find the motivation to master the tools that get you there.

— Eric Ong, CFA – Inspired by 這輩子賺多少才夠 by 黃士豪 Will Huang

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a Reply